What's happening in global freight

What to expect

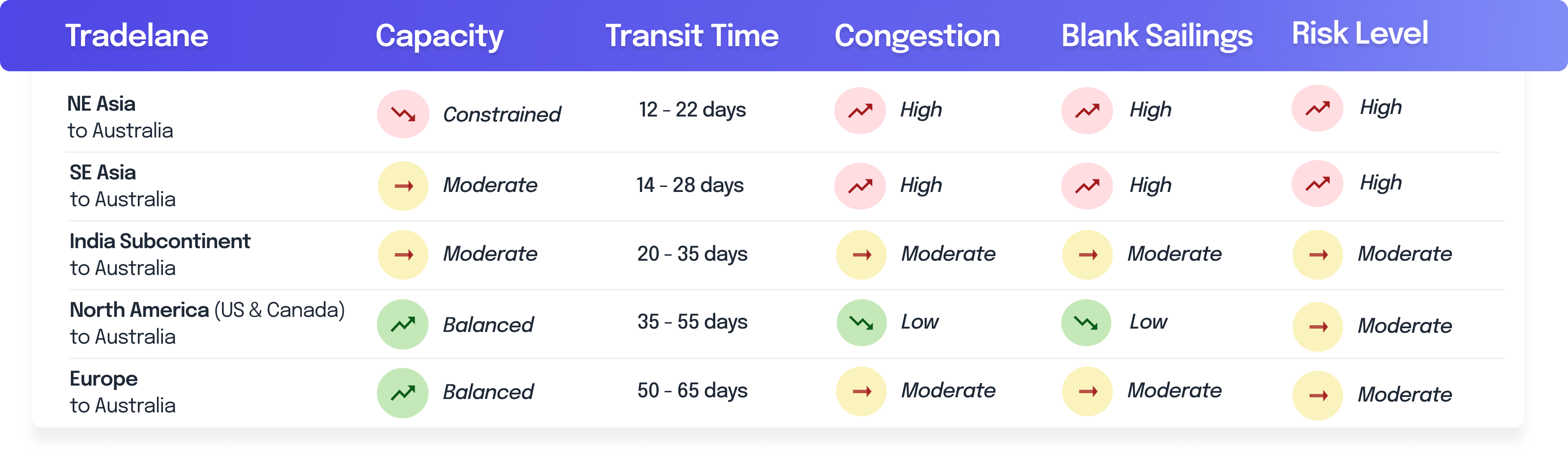

Global freight markets remain volatile, driven by ongoing geopolitical tension, rising fuel costs and continued schedule disruption across key trade lanes. Carriers are actively managing capacity through blank sailings and port omissions as they attempt to restore schedule reliability and support rate increases.

Singapore and major transshipment hubs remain congested, creating flow-on delays into Australia, while demand across Asia remains inconsistent. Despite softer global demand in some sectors, rates into Australia continue to trend upward due to vessel utilisation, operational disruption and increasing bunker-related surcharges.

Global freight rates

.png)

Key takeaways

- Rates are rising for Asian and Indian routes: Rates for NE Asia, SE Asia, and the India Subcontinent are all currently on an upward trend.

- US, Canada, and Europe routes are stabilising: In contrast to the Asian trades, shipping rates from the US, Canada, and Europe are showing signs of stabilisation.

- The "Why" behind the hikes: Even though global demand is a bit soft in some areas, rates are still climbing due to:

- Increased bunker-related surcharges

- Ongoing operational disruptions

- Carriers tightly managing capacity (using blank sailings and port omissions) to support these price increases

Global schedule reliability

Key takeaways

- Global schedule reliability improved to 62.2% in March 2026 according to Sea-Intelligence, however congestion, port omissions and ongoing delays across key transshipment hubs continue to impact service reliability into Australia.

Australia

Australia

Operational performance across Australia's major container gateways varies significantly heading into June. While ports like Brisbane and Adelaide are handling volumes smoothly with minimal disruption, East Coast hubs face moderate landside and terminal pressure, and Fremantle remains under the heaviest operational strain from vessel bunching and congestion.

Port of Brisbane

- Operating relatively smoothly overall

- Minimal vessel berthing delays currently reported

- Some minor landside pressure from rail and road networks

- Weather remains a watchpoint for QLD operations during peak rain events

- Low congestion indicators compared to other Australian ports

Port Botany

- Moderate congestion conditions continue

- Vessel bunching and schedule recovery measures impacting reliability

- Tight truck slot availability during peak periods

- Rolling risk elevated on some Asia-Australia services

- Terminal operations stable but under pressure from high import volumes

Port of Melbourne

- Moderate operational pressure remains

- Empty container park congestion still creating some landside inefficiencies

- Truck turnaround times improving versus prior quarters

- Webb Dock and Swanson Dock volumes remain strong

- No major widespread berth delays currently reported

Port of Fremantle

- Currently the most pressured major Australian container port

- Higher berth delays than East Coast ports

- Increased congestion linked to vessel bunching and schedule recovery

- Carriers building additional buffer into WA transit planning

- Landside operations still functioning but with tighter windows

Port of Adelaide

- Stable overall operating conditions

- Limited congestion reported

- Berthing windows generally holding

- Some indirect impact from delayed coastal vessel rotations

- Lower operational risk compared to larger East Coast gateways

North East Asia

North East Asia

Market conditions ex North East Asia into Australia remain unusually firm heading into June, despite this traditionally being a softer demand period linked to Australia’s EOFY slowdown.

Shipping lines have successfully implemented a further USD 300/TEU GRI from 1 June, with capacity tightening significantly across the first half of the month, particularly on services such as CAT, CAE and CA2.

Key market developments include:

- Total June sailings ex Shanghai to East Coast Australia sit at 40 sailings across 9 services, with 11 blank sailings currently scheduled, representing 27.5% capacity reduction.

- Blank sailings are more concentrated in the first half of June, where 33.3% of sailings are cancelled, compared to 22.7% in the second half.

- Premium services remain relatively stable, with blank sailings sitting at 22.2%.

- Kangaroo service is expected to withdraw from the Australia trade following the MSC MONTSERRAT 623A sailing on 7 June.

- PANDA and WALLABY services currently remain fully operational with no blank sailings.

- CAT/CAE/CA2 services continue to face the greatest disruption, with 42.8% of sailings blanked during June.

- Maersk/Hapag-Lloyd services remain stable, with no blank sailings and an additional vessel deployed mid-June to increase capacity.

Overall, carriers continue tightly managing capacity to support rate restoration efforts, with elevated rolling risk and reduced schedule reliability expected to persist throughout June, particularly on lower-cost service offerings.

Air Freight

Air freight conditions ex North East Asia into Australia continue tightening heading into June, driven by elevated fuel surcharges and subsequent airline flight cancellations reducing available capacity across the market.

Carriers are signalling further freight rate increases from June, with forward planning and earlier booking becoming increasingly important to secure uplift, particularly into Melbourne and Brisbane.

Key market highlights include:

- Capacity tightening across most major China gateways due to cancelled services and reduced flight frequencies.

- Freight rates continue trending upward across multiple carriers and trade lanes, particularly ex Guangzhou, Beijing and Hong Kong.

- Melbourne and Brisbane are experiencing the greatest pressure, with multiple airlines reporting tight space through late May and early June.

- Several carriers are limiting cargo profiles, prioritising smaller shipments or allocating space case-by-case.

- Additional operational disruptions include:

- China Airlines flight cancellations throughout June

- Reduced frequencies on select Hainan Airlines services

- Tight second-leg connections via Singapore Airlines and Malaysia Airlines

Some positive capacity developments include:

- Resumption of China Eastern 787 services into Melbourne from 28 May

- Additional uplift opportunities via Explorate ULD allocations into Sydney and Melbourne

- Select economy air products remaining comparatively stable on select lanes

Overall, the market remains firm with tightening capacity, rising freight rates and increasing pressure on available uplift into Australia as carriers continue actively managing networks and fuel-related operating costs.

South East Asia

South East Asia

.avif)

Market conditions ex South East Asia into Australia are sharing the same constraints as NEA with carriers actively managing capacity through blank sailings, space controls and rate restoration measures.

Key market developments include:

- Space availability remains tight across most direct and transshipment services into Australia, particularly on lower-cost service offerings.

- Carriers continue implementing blank sailings and schedule recovery measures to stabilise vessel intervals and support rate increases.

- Singapore and Port Klang transshipment hubs remain congested, contributing to ongoing schedule reliability pressure and extended transit times.

- Rolling risk remains elevated across both premium and economy services, particularly for late bookings and lower-rated cargo.

- Freight rates continue trending upward into June following recent GRI implementation, with further upward pressure possible if capacity remains constrained.

- Premium direct services continue performing more consistently, however vessel bunching and port omissions are still impacting schedule integrity across several loops.

- Australian port operations remain stable overall, although landside congestion and berth delays in selected ports continue impacting vessel schedules and container availability.

Air Freight

Air freight conditions ex South East Asia into Australia remain firm heading into June, with tightening capacity and rising freight rates across key export hubs including Singapore, Vietnam, Thailand, Malaysia and Indonesia.

Ongoing airline capacity management, elevated fuel costs and strong regional demand are continuing to place pressure on available uplift into Australia, particularly into Melbourne and Brisbane.

Key market highlights include:

- Space availability remains tight across most major South East Asia gateways, particularly for late bookings and larger cargo allocations.

- Freight rates continue trending upward as airlines manage reduced capacity and elevated operating costs.

- Singapore remains heavily congested across both ocean and air freight networks, impacting transshipment performance and connection reliability.

- Airlines are prioritising higher yielding cargo, with some carriers limiting allocations or confirming bookings closer to departure.

- Melbourne and Brisbane continue to experience the greatest space pressure across the Australian network.

- Transit delays are increasing on some indirect services due to tighter regional connections and schedule disruptions.

- Peak pressure remains concentrated around weekend departures and end-of-month uplift requirements.

- Forward bookings and early cargo readiness are becoming increasingly important to secure preferred flights and stable pricing.

India Subcontinent

India Subcontinent

.png)

Nhava Sheva (JNPA) is facing major disruption, with transport associations commencing an indefinite suspension of vehicle transport operations from 28 May in protest against rising LOLO charges at private empty container yards. The action is expected to halt empty container returns and restrict access to empty equipment for export shipments.

At the same time, the port has been under significant pressure over the past two weeks, with vessel delays of 2-5 days driven by Middle East cargo rerouting, trailer shortages and congestion across terminals. High yard density, limited export receival windows and ongoing driver shortages are also slowing import evacuations and inter-terminal movements.

Key market developments include:

- Space availability remains tight across several services into Australia, particularly on lower-rated cargo and late bookings.

- Carriers continue implementing selective blank sailings and port omissions to recover schedules and maintain vessel utilisation.

- Transshipment congestion through Singapore and Port Klang continues creating delays and extended transit times across the trade.

- Freight rates remain firm, with carriers attempting to maintain recent GRI increases and stabilise pricing through controlled capacity management.

- Rolling risk remains elevated on selected services, particularly during peak booking periods and on transshipment-dependent routings.

- Bangladesh export operations continue experiencing periodic congestion and infrastructure pressure, contributing to schedule volatility on some services.

- Schedule reliability remains below historical averages due to vessel bunching, port congestion and network recovery programs.

- Australian destination ports remain operational overall, although berth delays and landside congestion continue impacting vessel rotations and container availability.

Air Freight

Strong regional demand, constrained airline capacity and ongoing transshipment pressure through key Middle Eastern and Asian hubs are continuing to impact uplift availability and transit reliability into Australia.

Key market highlights include:

- Space availability remains tight across most major gateways, particularly for Melbourne and Brisbane bound cargo.

- Freight rates remain elevated, with airlines continuing to manage capacity conservatively across the market.

- Airlines are prioritising higher yielding cargo, with late bookings increasingly subject to rollover risk or premium pricing

- Weekend and end-of-month departures remain the most heavily constrained periods for uplift availability.

- Some carriers continue adjusting frequencies and allocations in response to fuel costs and network balancing requirements.

- Forward planning and early cargo readiness remain critical to securing preferred uplift and stable pricing outcomes.

Overall, the India Subcontinent air freight market remains tight, with constrained capacity, elevated rates and ongoing operational disruptions expected to continue through June.

North America

North America

Market conditions ex North America into Australia remain mixed, with stable demand levels continuing across the trade, however operational pressure and schedule disruption persist across several carrier networks.

While overall capacity remains more balanced compared to Asia-Australia trades, schedule reliability and inland network disruptions continue impacting transit consistency and cargo planning.

Key market developments include:

- Vessel schedules remain impacted by ongoing congestion and network recovery measures across parts of the US West Coast and inland rail networks.

- Port operations in Long Beach have stabilised overall, however intermittent congestion and berth window changes continue affecting vessel rotations.

- Inland rail delays and equipment imbalances across North America are continuing to impact container positioning and export planning.

- Freight rates remain relatively stable, although carriers are attempting to maintain pricing discipline through selective capacity management and reduced service flexibility.

- Rolling risk remains moderate, particularly on transshipment services and during peak booking windows.

- Schedule reliability continues below historical averages due to vessel bunching, port omissions and transshipment delays through Asia.

- Carrier focus remains on protecting utilisation and restoring schedule integrity following prolonged network disruption across global trades.

- Australian destination ports remain operational overall, although selected berth delays and landside congestion continue impacting vessel turnaround times.

Overall, the North America to Australia trade remains operational and relatively stable, however schedule disruption, inland transport pressure and transshipment congestion continue creating variability across transit times and service reliability through June.

Air freight

Air freight conditions ex North America into Australia remain stable overall, however capacity pressure and elevated operating costs continue impacting freight rates and uplift availability across key US and Canadian gateways.

Demand remains consistent across both general cargo and project-related freight, with airlines continuing to manage allocations closely on Australia-bound services.

Key market developments include:

- Space availability remains relatively balanced overall, however peak departure windows continue experiencing tighter uplift conditions.

- Freight rates remain elevated compared to historical averages, driven by fuel costs, network balancing and ongoing global capacity management.

- Transit reliability remains mixed, with some delays occurring through major transshipment hubs across Asia and the Middle East.

- US West Coast gateways continue operating steadily overall, although inland trucking and rail disruptions are periodically impacting cargo flows to airports.

- Airlines are maintaining disciplined capacity management, with some carriers reducing flexibility for late bookings or oversized cargo.

- Melbourne and Brisbane continue experiencing tighter uplift availability compared to Sydney on selected services.

- E-commerce and technology-related cargo continue contributing to stable outbound demand from North America.

- Forward planning remains important, particularly for larger shipments and end-of-month departures where capacity tightens quickly.

Overall, the North America to Australia air freight market remains operational and relatively stable, however elevated rates, constrained peak-period capacity and ongoing network disruption continue impacting transit consistency into Australia through June.

Europe

Europe

.png)

Market conditions ex Europe into Australia remain challenging, with ongoing schedule disruption, transshipment congestion and extended transit times continuing to impact reliability across the trade.

Carriers continue actively managing networks through schedule recovery measures and selective capacity controls as operational pressure across Europe and key transshipment hubs persists.

Key market developments include:

- Schedule reliability remains below historical averages, with vessel bunching and port omissions continuing across several services.

- Congestion across major European ports and transshipment hubs, particularly Singapore and Port Klang, continues impacting transit consistency into Australia.

- Blank sailings and service adjustments remain present across selected carrier networks as lines attempt to stabilise schedules and protect utilisation.

- Freight rates remain relatively firm despite softer overall global demand, supported by controlled capacity management and elevated operating costs.

- Rolling risk remains moderate across the trade, particularly for transshipment cargo and late bookings.

- Ongoing Red Sea disruption continues impacting vessel routing decisions, network planning and transit times for Europe-Australia services.

- Equipment availability remains generally stable, although selected inland European locations continue experiencing periodic container and trucking constraints.

Overall, the Europe to Australia trade remains operational but under ongoing schedule pressure, with congestion, network recovery measures and geopolitical disruption continuing to impact transit reliability and carrier performance through June.

Air freight

While overall network stability has improved compared to previous quarters, congestion through major transshipment hubs and operational disruption across parts of Europe continue impacting transit consistency and uplift availability.

Key market developments include:

- Space availability remains relatively stable overall, however tighter conditions persist during peak departure periods and on Australia-bound connections.

- Freight rates remain elevated compared to historical norms, supported by fuel costs, constrained global capacity and ongoing network balancing.

- Transit reliability remains mixed, with some delays occurring through major hubs including Dubai, Singapore and Doha.

- Airlines continue prioritising higher yielding cargo, with late bookings increasingly subject to reduced flexibility or premium pricing.

- European airport operations remain stable overall, although periodic congestion and handling delays continue impacting selected gateways.

- Capacity into Melbourne and Brisbane remains tighter compared to Sydney across several carrier networks.

- Ongoing geopolitical instability and airspace disruptions linked to the Middle East continue influencing airline routing and operating costs.

- Forward planning remains important for larger shipments, project cargo and end-of-month uplift requirements.

Overall, the Europe to Australia air freight market remains stable but firm, with elevated freight rates, tighter peak-period capacity and ongoing transshipment disruption expected to continue through June.

Key takeaways

.avif)

Experienced Business Development Manager with a demonstrated history of working in the logistics and supply chain industry. Skilled in Import/Export, Freight Transportation, Freight, Warehouse Operations, and Overseas Networking.

Frequently Asked Questions

Explorate gives supply chain managers one real-time view across ever forwarder, lane and mode without replacing your current process, partners or systems.