Upcoming Public Holiday in Brisbane: Wednesday 13th Of August - Ekka Show Day

Australian Terminals:

Sydney (Airport)

Qantas Freight has wrapped up its terminal upgrades at Sydney’s Kingsford Smith Airport, and it’s good news for efficiency and capacity. The revamped facility now includes additional temperature-controlled storage (with brand-new cool and ambient rooms), upgraded roller doors, and a fully automated roller deck system. A new bypass lane has been added to ease traffic flow on-site, and there's an improved landside-to-airside interface to streamline cargo movement. All in all, a solid step forward in improving freight handling speed and reliability.

Fremantle

Fremantle Ports has announced a fee adjustment kicking in from October 1, with increases to mooring and Terminal Handling Charges. While the change is relatively minor, it’s likely carriers will pass this through to shippers, so you may notice a small uptick in costs. For clarity around how this affects your shipments, please touch base with your Client Success Manager or Service Specialist.

Fremantle was also hit by severe weather in early July, forcing a full two-day terminal shutdown and anchorage delays. Following this, the Harbour Master reminded all operators of the importance of regularly reviewing their Adverse Weather Management Plans, especially with increased risks of strong winds and gales this time of year. For operational continuity, it’s worth reviewing the Port Information Guide 2025 and HMOP 04 procedures.

Brisbane

Brisbane terminals have seen some disruptions in July, mostly tied to system upgrades. DP World rolled out its new Optibook platform, which caused a full terminal closure on July 10 and a second short outage on July 16. Patrick's Terminal was also affected by shutdowns on July 13 and 22. The delays were minor but worth noting if you experienced any hold-ups on cargo ex-Brisbane.

Adelaide

There’s some welcome industrial relations stability out of Adelaide. Flinders Adelaide Container Terminal has reached an in-principle Enterprise Agreement with the Maritime Union of Australia, covering stevedoring workers until March 2029. The deal is still being finalised before submission to the Fair Work Commission, but it’s a positive move for long-term planning and operational consistency at the port.

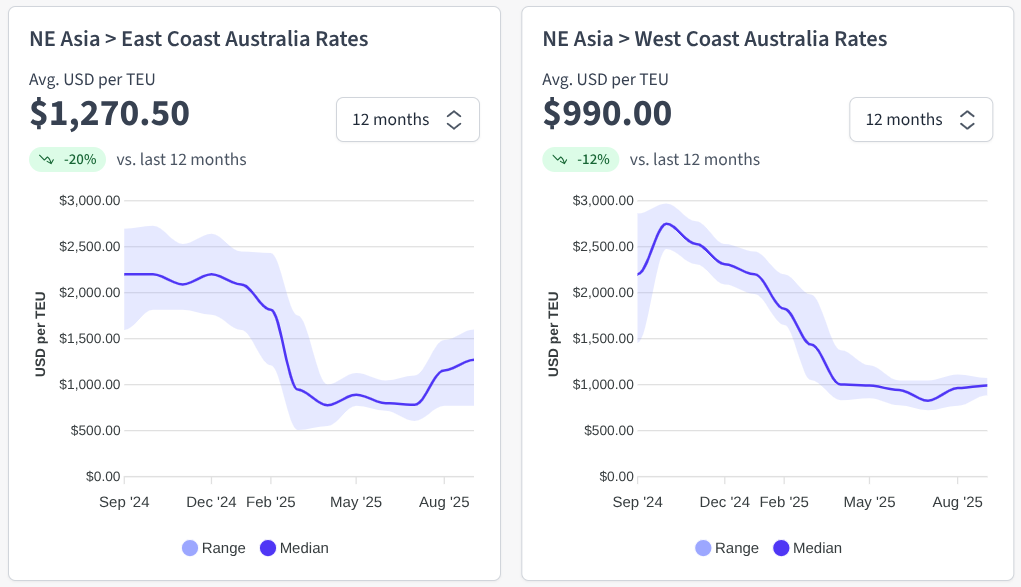

It’s a turbulent time across the Asia Pacific corridor, with the usual seasonal chaos ramped up by blank sailings and serious congestion in major ports like Shanghai and Busan. Rates are feeling the pressure and climbing, especially now that carriers have managed to push through significant increases, finally hitting four-digit figures.

Schedules are still messy, with some vessels arriving just days apart. This has led some carriers to throw in last-minute rate incentives just to keep boxes moving. Typhoon season isn’t helping either; weather disruptions are causing ripple effects across already strained schedules.

With Golden Week on the horizon (Oct 1–7), demand is expected to lift further. Carriers are already implementing GRIs of USD 300–500/TEU from August 1, and some are layering on Peak Season Surcharges of USD 350/TEU. Space is tightening fast; if you’ve got cargo to move, now’s the time to lock it in and avoid the premium price tag later.

With August firmly in peak season, carriers aren’t expecting any major price drops and are instead carefully testing the market. Each carrier is focused on maximizing profits while keeping its ships full, often overbooking its vessels. This strategy helps them stay flexible amid market fluctuations and is why we’re seeing rollover rates climb, especially at South China ports.

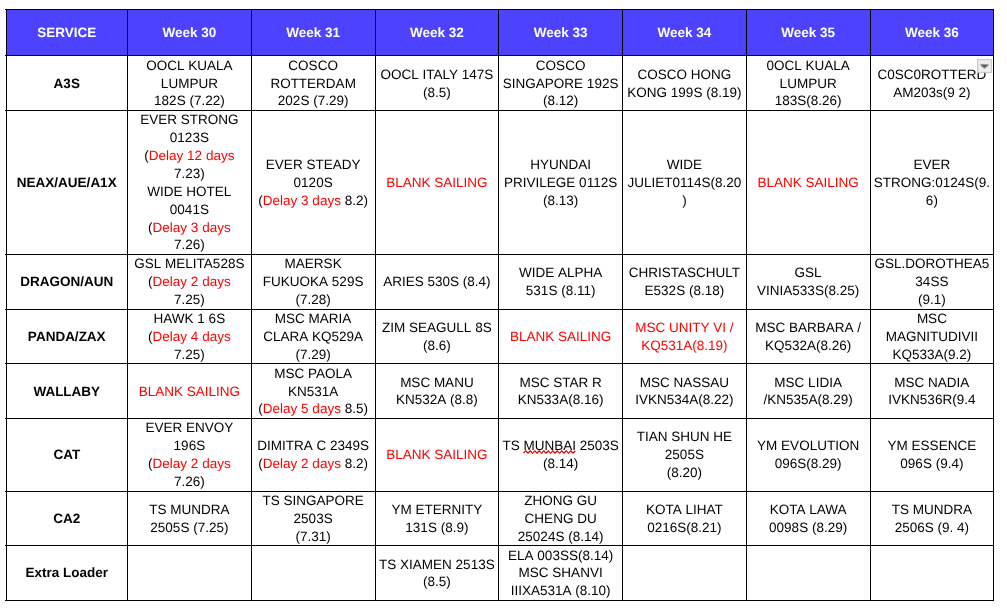

Although the early-month ad-hoc vessel TS XIAMEN 2513S added only around 1,500 TEUs of extra capacity (quickly absorbed by the market after TSL introduced promotional rates), the upcoming departure of TS MUMBAI 2503S (under the CAT service) from Shanghai around August 10th aligns with the arrival of a much larger 7,092 TEU vessel. This unexpected capacity surge has shifted the previously balanced supply-demand equation for the second week of August into oversupply.

Most Competitive Services: These carriers acted swiftly to ensure full vessel utilization, taking the lead by reducing rates on all sailings from major Chinese ports between 8th and 14th August under their CAT/CA2 services. Base rates dropped from USD 1,300 / 2,600 to USD 1,200 / 2,400 per 20’/40’. Other major carriers quickly followed suit, implementing similar downward adjustments. Maersk (MSK) entered the market aggressively, offering the lowest rate for the week: USD 1,150 per 20GP and USD 2,300 per 40HC.

Mid-Tier Services: Mid-Tier carriers are aligning with the market trend, and have revised their rates to USD 1,300 per 20GP and USD 2,600 per 40HC, reflecting an aggressive and competitive position. Panda/ZAX services recently adjusted rates to USD 1,250 per 20GP and USD 2,500 per 40HC, placing them strategically between the CAT/CA2 and NEAX (A1X) service tiers.

Premium Services: Confirmed no intention to adjust rates for the second week of August, citing strong load factors. Their final rates remain firm at USD 1,450 / 2,900 per 20’/40’, effective from August 8 to 14, covering all major China ports. The A3 service has been in high demand, with space allocation tightly held.

Advertised GRIs:

ANL: USD500.00 per TEU Rate Restoration (GRI) for all shipments effective 15th August 2025, ex Asia, Indian Sub-Continent & Middle East to Australia.

Maersk: Peak Season Surcharge (PSS) of USD300.00 per TEU for shipments from China, Japan, South Korea, Hong Kong, Mongolia, Cambodia, Laos, Myanmar (Burma), Thailand, Vietnam, Brunei, Indonesia, Malaysia, Philippines, Singapore, Timor Leste to Australia, effective 4th August 2025.

Maersk: Peak Season Surcharge (PSS) of USD300.00 per TEU for shipments from Taiwan to Australia, effective 18th August 2025.

MSC: Rate Restoration (GRI) of USD300.00 per TEU for all cargo from China, Hong Kong, Taiwan, Japan, Korea, Cambodia, Thailand, Vietnam, Malaysia, Myanmar, Singapore, the Philippines, and Indonesia to Australia and New Zealand. Effective 15th August 2025.

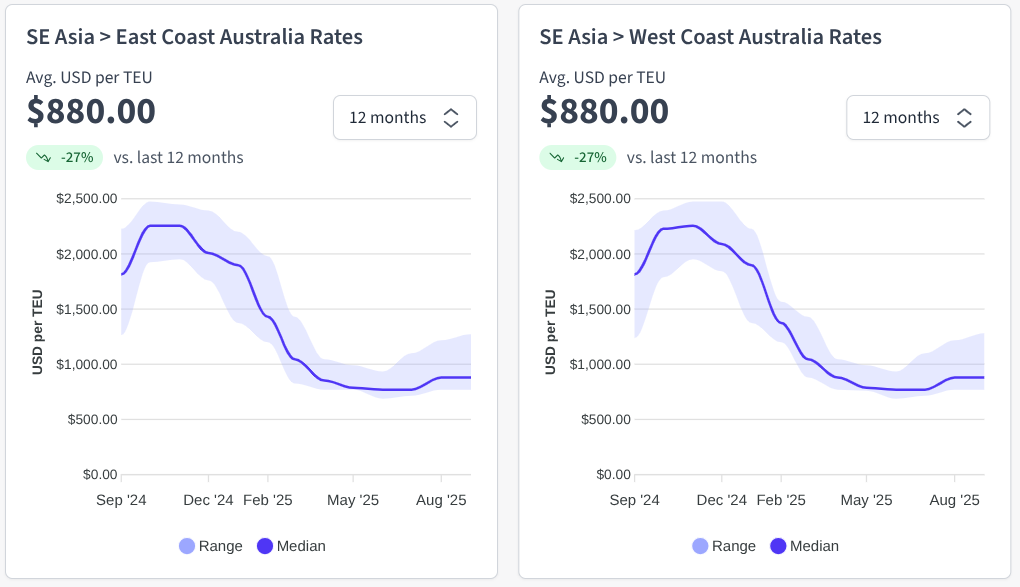

Compared to Northeast Asia, the Southeast Asia market is holding relatively steady on rates, though capacity is tightening. Delays with feeders and ongoing equipment shortages at transshipment hubs like Singapore and Port Klang are starting to bite.

Export volumes out of Vietnam and Thailand are picking up slowly, reflecting a gradual rebound in demand. While many carriers have announced General Rate Increases (GRIs), market pushback has kept them from sticking across the board. Peak Season Surcharges (PSS) are floating around but remain moderate and vary depending on the line.

Expect potential short-term rate hikes and PSS adjustments throughout August, driven by equipment imbalances and growing congestion at key transshipment points. Schedule reliability will remain touch-and-go until equipment repositioning improves.

Capacity:

ANL is introducing an extra vessel in week 33.

Ela V. 003SS / 1750 TEU

SHA 11/Aug - SHK 14/Aug - SYD 30/Aug - MEL 02/Sep

TS Lines is introducing an extra vessel in week 32.

MSC is introducing an extra vessel in mid-August (TBC)

MSC Shanvi III V.531A / 3534 TEU

Departing from TAO or SHA

We’re currently facing significant space challenges ex-China and Vietnam, with tight capacity being felt across the broader Asian region. Securing confirmed bookings has become increasingly difficult, often taking one to two weeks - and even then, there’s a high risk of rollovers due to ongoing vessel overbookings by carriers.

Many shipments are being rolled at origin, and congestion is further compounding delays by pushing vessel ETDs out. The recent typhoon activity in China has also led to temporary wharf closures, halting all movements until weather conditions stabilise. This is expected to impact connecting transhipment vessels and may result in increased port rotations or omissions at destination.

Space out of Malaysia is extremely tight. Some carriers are fully booked throughout August, with spot options in high demand. Book 4 weeks ahead.

Blank Sailings

ANL is releasing a new service – APR 2 – connecting North Asia, PNG, and Far North Queensland:

Start Date: Service begins 12th September 2025

Vessels & Frequency: Operating 3x1700 TEU vessels on a 14-day frequency.

We're seeing widespread delays across Asia due to seasonal weather events - typhoons, monsoons, and everything in between. These conditions are impacting vessel schedules and contributing to ongoing congestion at several key ports.

Locally, strong winds - typical for this time of year - are causing intermittent closures of empty container yards and wharves as safety assessments are conducted. This is delaying vessel discharge operations and contributing to port omissions or last-minute changes in port rotations as carriers work to recover their schedules.

Equipment shortages persist ex China, with vessel waiting times of up to 5 days.

Click image to start tracking

Due to adverse weather conditions expected to affect shipping movements at the Port of Brisbane, AAXE vessel MAERSK FREMANTLE 529S will omit the Brisbane southbound call to mitigate delays, along with any further disruption to the schedule. Brisbane cargo will remain onboard the vessel through Sydney and will now discharge on the Brisbane northbound call (import voyage remains 529S). Source: ANL

ALS CLIVIA 001N is experiencing a serious delay in her schedule, and in order to assist with schedule recovery, ALS CLIVIA 001N will omit the Sydney call. Source: ANL

Due to port congestion in Shanghai, OOCL BRAZIL 049N/050S will omit Xiamen in order to assist with schedule recovery. Source: ANL

The vessel HAWK I V6S will omit Brisbane on the southbound call. This will now call Melbourne first, and Brisbane on the northbound call.

Indian Subcontinent

Chittagong The port continues to struggle with heavy congestion. Ships are waiting 6 to 8 days to dock, with some vessels waiting as long as 10 days. Yard capacity is stretched, and waterlogged areas are slowing down operations even more. On top of that, a shortage of locomotives is causing rail cargo bound for Dhaka ICD to sit for three weeks or more before moving.

Colombo, Sri Lanka Monsoon conditions are wreaking havoc on Colombo’s port operations, especially given its role as a major transshipment hub. The number of vessels waiting at anchor hasn’t improved. High yard occupancy and logistical challenges moving containers between terminals mean delays are piling up. Expect transshipment shipments to be held up by one to two weeks.

India Monsoon rains are causing interruptions at Mundra, Kandla, and Nhava Sheva ports. Vessel schedules are being affected by weather pauses, which are adding to delays across the region.

Rates:

TPEB: The August 1 General Rate Increase (GRI) has been pulled back, and the Peak Season Surcharge (PSS) is officially off the table for August.

Rates for the first half of the month are being held steady, with even more relief showing on East Coast and Gulf lanes.

This shift is being driven by flat demand and the full removal of PSS in the fixed market.

Spot rates on Transpacific routes dropped again this week. Shanghai–Los Angeles fell 2% to $2,632/FEU, and Shanghai–New York also slid 2% to $4,135/FEU. With the pre-tariff rush now behind us and the temporary pause on higher U.S. tariffs ending mid-August, carriers are starting to pull back capacity by blanking more sailings. As a result, we’re likely to see a more stable rate environment in the short term. Source: Drewry

Capacity:

TPEB: August demand is tracking right in line with July – steady but not spiking. Capacity is sitting around 70–80% of normal levels, with no major cuts announced. This means the market is still heavy on space compared to current volumes.

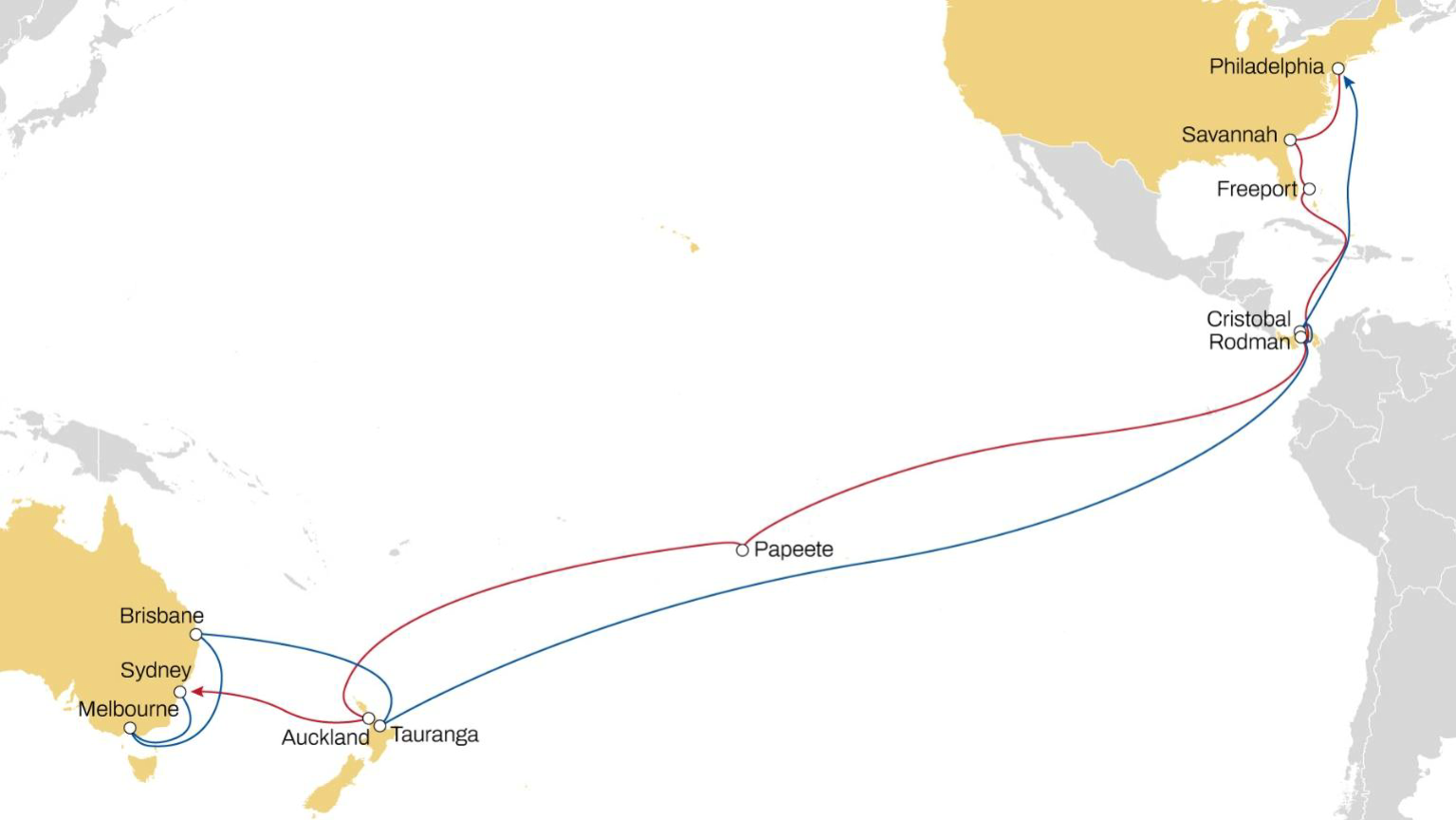

MSCis excited to announce that it will launch an enhanced standalone Eagle Service fromAustralia/New Zealand to USA East Coast commencing February 2026.

MSC will deploy 11 vessels on this weekly rotation. This new service will also provide connections through Panama to and from Europe, Central and South America, as well as USA Gulf ports.

The service will call at the following ports:

Philadelphia – Savannah – Freeport – Rodman – Papeete – Auckland – Sydney – Melbourne – Brisbane – Tauranga – Rodman – Cristobal – Philadelphia

Schedule Reliability:

TPEB: Space availability has actually improved slightly since late July, but equipment challenges are still hanging around. CMA and HMM are feeling it the most, while other carriers are showing better balance.

Typhoons hitting Ningbo and Shanghai this week have paused empty container pickups and are expected to cause some vessel delays.

Key updates for Australian businesses (as at 6th August 2025):

De minimis exemption ends globally on 29 August – All low-value imports (under $800) will now face tariffs, disrupting online retail and low-cost sourcing.

New 50% tariffs – Copper and Brazilian goods now face 50% duties; pharma and BRICS nations may be next.

India tariffs live – 25% tariff on Indian imports began 1 August.

EU deal in progress – Proposed 15% U.S. tariff on EU autos, pharma, and semiconductors.

No tariff workarounds – Transshipped goods won’t escape new rates.

FEWB: August FAK levels are holding firmer, sitting around 5–8% higher than the back half of July. With vessel utilization already running high in early August, rates have some upward pressure, especially as we move towards September. The Shanghai Containerized Freight Index is showing signs of climbing, and with Maersk’s recent PSS announcement on long-term deals, other carriers are beginning to shift their surcharges in anticipation of peak season demand.

TAWB: Carriers in Northern Europe and the West Mediterranean have held off on the PSSs that were planned for July, keeping rates stable for now. This steady pricing trend is expected to carry through the end of Q3. In the East Mediterranean, some carriers are starting to roll out GRIs for September, hinting at potential movement as we approach the next quarter.

While specific European rates weren’t highlighted this week, the broader WCI trend suggests that volatility has eased across the board. With the market finding its footing again, we can expect more predictable movement on the Asia–Europe lanes, especially as capacity and demand begin to rebalance. Source: Drewry

Capacity:

FEWB: Space for the first half of August has tightened quickly, with demand tracking steady. The real surge is expected to hit in late August as major retailers start locking in bookings ahead of September volumes, which could push utilization even higher.

TAWB: Capacity is holding steady with blank sailings easing back to around 4–7%, a noticeable month-over-month drop. While vessel space isn’t the key challenge at the moment, landside bottlenecks are putting pressure on the network. Antwerp is still experiencing its worst congestion since COVID, with dwell times stretching beyond eight days and yard utilization over 90%. Rotterdam, Hamburg, and Bremerhaven aren’t far behind with utilization sitting in the 80–85% range and resulting in two to four day vessel delays.

FEWB: There’s been a slight improvement in space availability since late July, but equipment imbalances are still an issue for CMA and HMM while other carriers are seeing better stability. Typhoons affecting Ningbo and Shanghai have paused empty container pickups this week, and we’re likely to see some vessel delays as a result.

TAWB: Piraeus, Genoa, and Valencia continue to report heavy yard overcrowding, keeping vessel wait times between two and five days—a pattern that’s been holding since the spring. River level drops, strike actions, and ongoing rail disruptions are compounding delays across Europe. On top of that, container and chassis shortages remain persistent in Austria, Slovakia, Hungary, Southern and Eastern Germany, and Portugal, with no sign of improvement yet.

Germany Major changes are coming to German ports from 1 October 2025, with the current PIN-based container release system being replaced by a fully digital “secure release order.” This closed-loop, authorisation-based process will streamline and secure container pickups across Hamburg, Bremerhaven, and Wilhelmshaven. Operationally, the situation in Hamburg and across the northern rail corridors remains strained. Ongoing infrastructure congestion has led to severe train delays and slot cancellations, impacting both import and domestic connections. The complete closure of the A59 between Duisburg-Nord and Duisburg is expected to further slow trucking from 29 July to 26 August, with phased closures in both directions. Hamburg terminals remain under pressure, with full berthing lineups and heavy yard utilisation. CTB is seeing vessel waits of up to 2 days, while CTT continues to enforce truck delivery restrictions. Labour shortages are expected to persist through September.

Belgium Yard congestion is still an issue with vessel waiting times up to 2 days and barge delays between 48–72 hours. Truckers are advised to use off-peak hours to avoid delays of up to 1 hour during peak. Labour availability drops further on weekends.

Netherlands ECT and RWG terminals are facing significant congestion. At ECT, berthing delays for late vessels are around 2 days, and barge delays are at 24–48 hours. RWG is seeing the worst congestion in the region, with average vessel wait times of 10 days and barge delays stretching to 72 hours. Imports should be collected as soon as possible to ease yard pressure. Rail restrictions will also affect operations between 2–4 August due to construction.

Italy The Port of Genoa is heavily impacted, with vessel waiting times up to 3.5 days and some port omissions being reported. Yard density is at 90%, and labour shortages are causing operational delays. Further rail disruptions are expected in August across La Spezia, Livorno, and Ravenna routes. Meanwhile, Maersk has officially commenced calls at the Port of Milazzo, Sicily. Its vessels will now be handled at the private Duferco Terminal Mediterraneo, which supports various container types, including reefers and IMO cargo.

Spain Congestion continues across key Spanish ports. Valencia is the most affected, with waiting times now exceeding 3 days and 15 vessels queued at berth. In Barcelona, delays are up to 36 hours, while Algeciras remains heavily utilised with vessels waiting up to 1.5 days.

United Kingdom Vessel diversions have slightly eased port congestion, but productivity remains low due to recent power and system outages. Dredging works are still underway, and while current waiting times are more manageable, performance remains below optimal levels.

Global Overview:

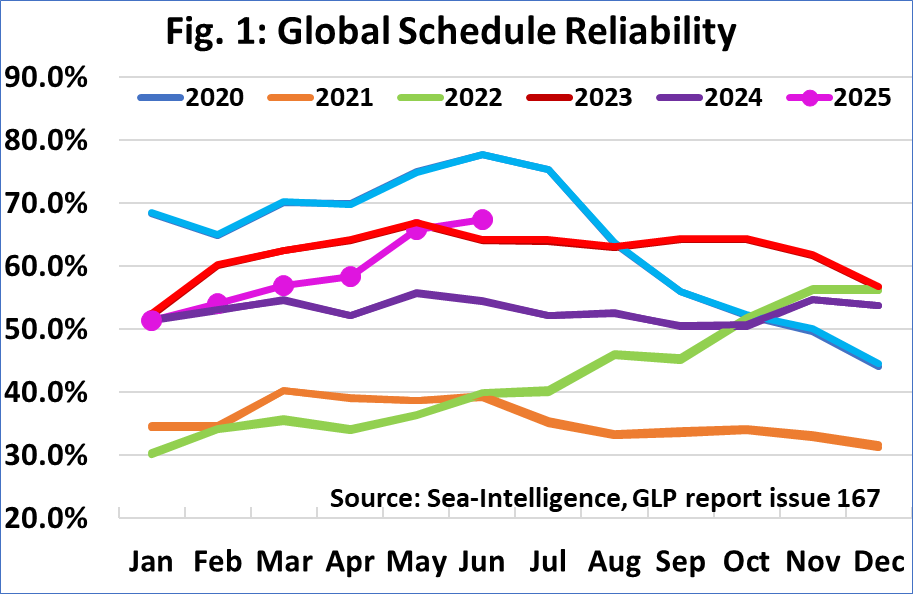

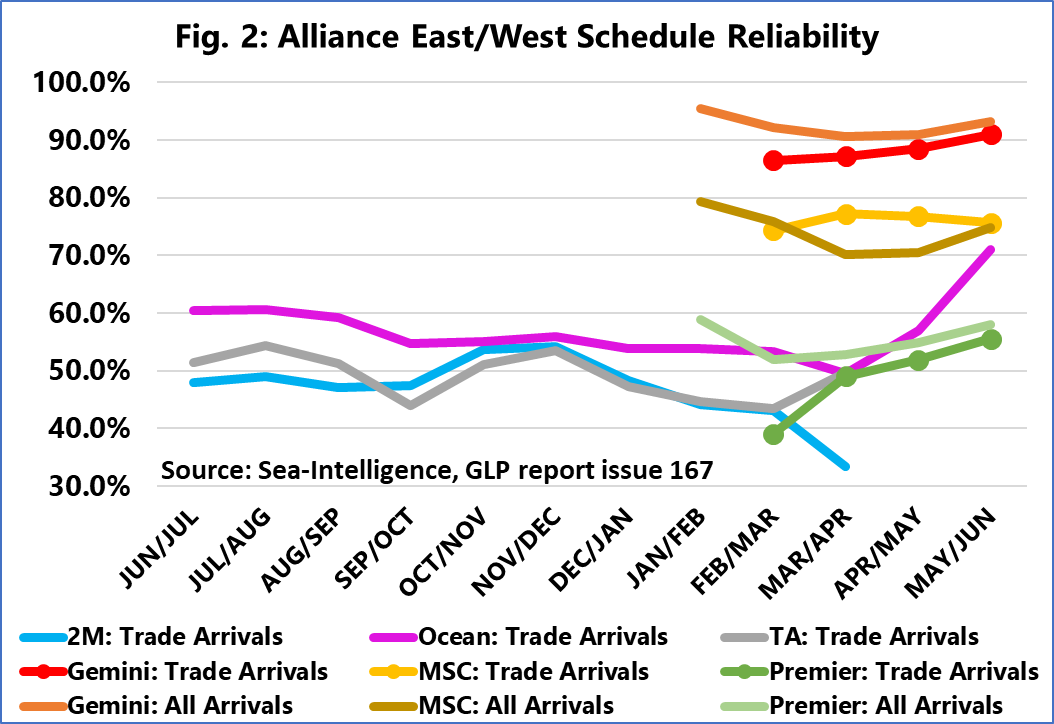

Schedule reliability continued to trend in the right direction in June, climbing another 1.6 percentage points month-on-month to hit 67.4%. That’s the highest level we’ve seen since November 2023, marking five straight months of improvement.

Year-on-year, reliability has jumped by 12.8 points. Maersk led the pack in June with 81.0% reliability, closely followed by Hapag-Lloyd at 76.5%. Most of the top players sat in the 60-70% range, while a few lagged behind - Yang Ming came in at the bottom with 55.4%. Source: Sea Intelligence

Because the usual alliance performance data - based only on destination arrivals - wasn’t available when the new alliances launched back in February, a broader metric was introduced. Instead of tracking just trade-lane endpoints, we now also include origin port calls across East/West trades. We’re continuing to show both sets of figures: “All arrivals”, which includes every port call and matches the February approach, and “Trade arrivals”, which aligns with the legacy methodology. Once the new alliances are fully bedded in, these two numbers should start to align.

In May and June 2025, Gemini Cooperation led the way, posting 93.2% schedule reliability on all arrivals and 91.0% on trade arrivals. MSC followed with 74.8% and 75.7% respectively. Premier Alliance came in significantly lower, with 58.0% for all arrivals and 55.5% on trade arrivals. For the original alliances, there’s no difference between the two measures - Ocean Alliance held steady at 71.0%. Source: Sea Intelligence

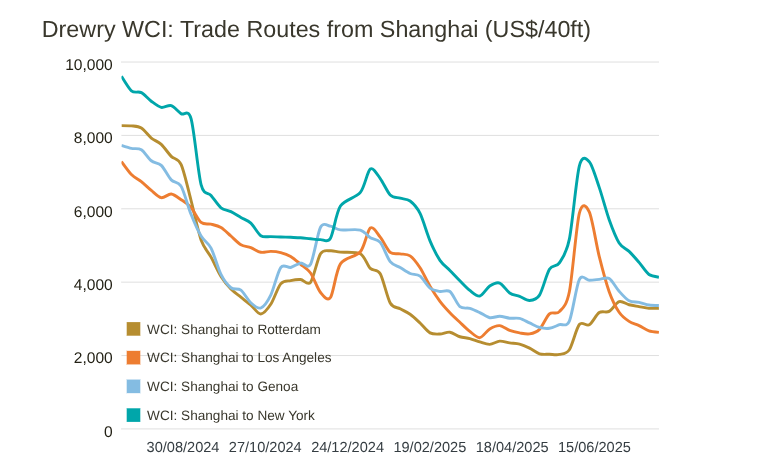

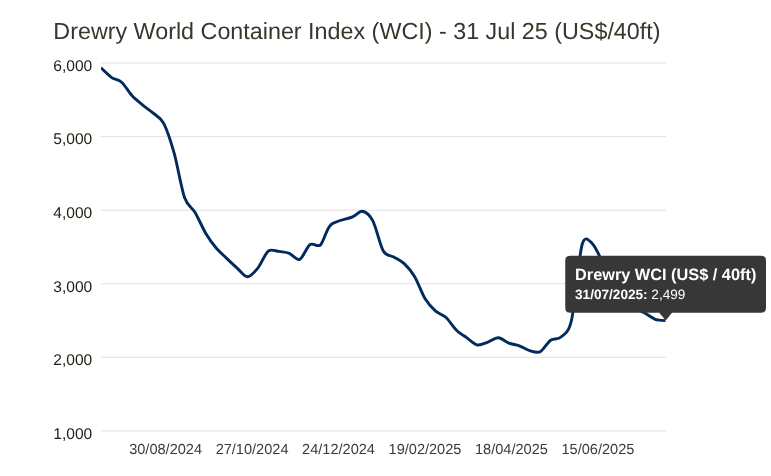

Drewry’s World Container Index (WCI) dipped just 1% this week, showing signs of stabilisation after a few months of sharp swings. Rate volatility kicked off in April following the U.S. tariff announcement, which triggered a surge through May and early June. That was followed by a steep correction through mid-July, but over the past couple of weeks, the pace of decline has eased noticeably. Source: Drewry

In late July (week 30, July 21–27), global air cargo markets settled into relative stability after weeks of turbulence triggered by U.S. trade policy and tariff shifts. On a worldwide basis, tonnages and rates held largely flat.

Asia Pacific to U.S. volumes bounced back - flown weight from China rose 4 % week-on-week (WoW), and from Hong Kong, +5 %, recovering from the prior-week declines caused by Typhoon Wipha’s cancellations. That recovery helped lift overall Asia Pacific → U.S. tonnage gains to around +3 % WoW for the market as a whole. Spot rates on this lane ticked up modestly, to US $4.89/kg, a 2 % WoW increase. Meanwhile, South Korea → U.S. rate volatility reversed dramatically - a 17 % drop in week 29 was met with a 29 % rebound in week 30, bringing rates to US $6.01/kg—their second-highest level this year.

By contrast, Asia Pacific → Europe flows remained subdued. Hong Kong → Europe volumes saw only a +2 % rebound after a 7 % fall the week before, and China → Europe tonnages dipped a further 2 %. Overall, Asia Pacific → Europe tonnage declined about 2 % WoW in week 30, with Japan hardest hit, down 10 %.

Looking at broader origins, European export volumes in week 30 rose about +3 % WoW, while chargeable weight from the Middle East & South Asia dropped 3 %, and North America declined 2 %. Pricing was also flat across those origins - worldwide average rates edged up just 1 % WoW, reaching around US $2.45/kg, nearly matching the same week last year. Spot rates were similarly steady (+1 % WoW to US$2.66/kg), though still 1 % below year‑ago levels. Africa-origin spot rates showed the biggest volatility - dropping 11 % WoW, after a 13 % spike the week before.

On a year‑on‑year basis, week 30 chargeable weights were up 5 % from the prior year. Every major region posted gains: Asia Pacific led with +7 %, Central & Latin America +5 %, and Europe +3 %. Pricing remained modestly higher overall - just about +1 % higher than year‑ago rates. However, the Middle East & South Asia region saw more pronounced rate reductions - averaging an −11 % drop in full‑market rates and a 20 % decline in spot prices YoY. Source: World ACD

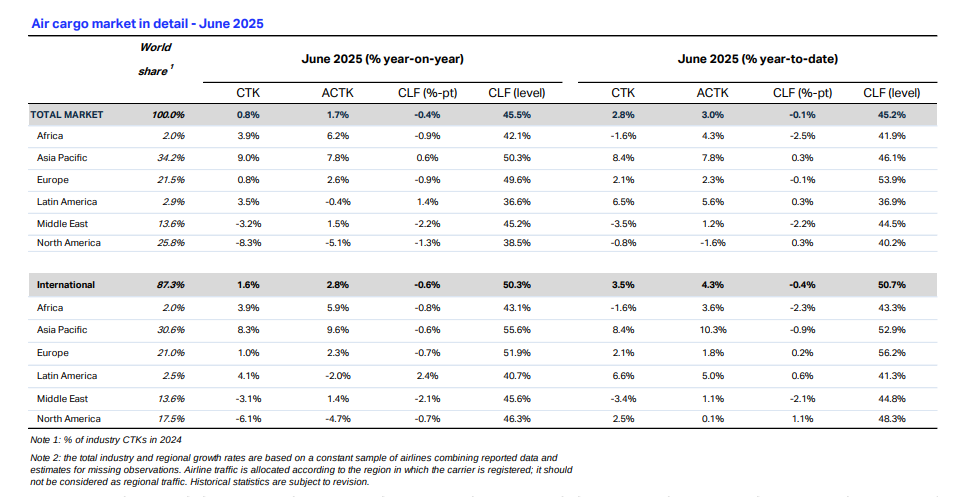

IATA Overview:Air cargo demand grew just 0.8% year-on-year in June, down from 2.2% in May, as the market absorbed continued trade uncertainty and tariff-driven disruption. Capacity (ACTK) expanded 1.7% YoY, while cargo load factor (CLF) slipped by 0.4 percentage points to 45.5% - a sign that carriers are recalibrating space to match the softer demand environment.

Regional Performance: Asia-Pacific led the way with +9.0% YoY growth in cargo volumes and a CLF around 50.3%, reflecting strong intra-regional and export flows. Europe posted modest growth (+0.8% CTK, CLF ~49.6%). North America showed the weakest performance, down 8.3% YoY, with CLF dropping to 38.5%. Middle East and Africa volumes also contracted, while Latin America rebounded with modest gains.

Trade Lanes & Outlook: Asia–Europe trade continued its long growth streak with +10–11% YoY, while the transatlantic lane (Europe–North America) climbed +4.8%. In contrast, flights between Asia and North America slipped again, showing another month of decline (–4.7% YoY). Fuel costs dropped 12% YoY, easing pressure on operators, though freight yields fell ~2.5% YoY despite a small uptick (+0.9%) month-on-month.

Macro Overview: IATA has trimmed its 2025 air cargo forecast to 69 million tonnes (+0.6% YoY), compared with earlier projections of 72.5 million tonnes, and expects cargo revenue to drop 4.7% to $142 billion. Ongoing trade frictions, supply chain strain, and aircraft delivery delays - now reaching record backlogs - remain core headwinds for the sector’s outlook.

General News.

2025/26 BMSB (Brown Marmorated Stink Bug) Season will commence on 1st September - 30 April (inclusive). There are 41 current target risk countries, with the UK and China now considered as emerging risk countries. Random inspections will apply to goods shipped from the United Kingdom and China between 1 September to 30 April (inclusive). In addition to the target high-risk goods, chapters 39, 94, and 95 will be subject to random inspections for emerging risk countries only.. You can find full details at the DAFF website.

Typhoon Co-may made landfall in eastern China on Wednesday, hammering Shanghai, Zhejiang, and Jiangsu with torrential rain and fierce winds. Shanghai was hit twice - once in the early morning and again in the afternoon - prompting mass evacuations of over 283,000 people, flight cancellations, and the shutdown of thousands of construction sites. Emergency response protocols were activated, and major disruptions affected air, rail, and ferry transport. While the metro system stayed online, authorities implemented speed limits on highways and temporarily closed tourist attractions like the Shanghai Tower’s observation deck. Though not the strongest storm by wind speed, Co-may's slow movement meant extended rainfall, heightening the risk of flash floods, landslides, and urban waterlogging. Zhejiang issued a red geological disaster alert, and Jiangsu raised its heavy rain warning to yellow. A tsunami warning caused by an offshore earthquake was briefly in effect but later lifted. With the typhoon still moving northwest, officials are maintaining a high alert and warning residents to avoid high-risk areas like mountains and rivers, even after the rain stops. Source: China Daily

Mount Lewotobi Laki‑Laki erupts again with force in early August, sending plumes of ash soaring into the sky. The volcano on Flores Island erupted Friday evening and again under five hours later, blasting ash up to 18 km (11 miles) high and blanketing nearby villages in debris. Pyroclastic flows raced down slopes, and glowing lava and lightning lit up the night sky. Thankfully, no casualties have been confirmed so far. Authorities have maintained the volcano at the highest alert, expanded the exclusion zone to around 7 km, and reinforced warnings about potential mudflows triggered by rain. Although transportation disruptions have been limited — the June ash cloud previously grounded flights into Bali — livelihoods remain at risk as the heightened activity continues. Source: CNN

The Krasheninnikov Volcano on Russia’s remote Kamchatka Peninsula erupted on August 3, 2025, marking its first activity in around 600 years. The eruption sent ash plumes nearly 4–6 km into the sky, prompting researchers in the area to evacuate, though no injuries were reported. Fortunately, the volcano sits within the Kronotsky Nature Reserve, far from populated regions, keeping its impact on daily life minimal.Scientists believe this eruption is linked to a powerful 8.8-magnitude earthquake that struck just days earlier. That same seismic event also triggered eruptions at other nearby volcanoes, including Klyuchevskoy. Ash from the blast drifted over the Pacific, triggering elevated aviation alerts, but posed no immediate threat to communities. Source: BBC

An Evergreen Marine vessel, the Ever Lunar, lost around 50 containers overboard while anchored off the Port of Callao in Peru on August 1. The ship had been waiting to enter the port when it rocked suddenly, possibly due to tsunami waves linked to a major Russian earthquake, bad sea conditions, or rogue wave activity, which caused containers stacked at the stern to fall into the bay. All crew members were reported safe, and no hazardous materials were aboard the lost containers - authorities confirmed they mainly carried plastic goods. The incident triggered a temporary closure of the port, halting operations across key terminals until visibility improved and floating containers were marked. Recovery operations using buoys and cranes are underway, with port reopening expected later in the day once safety conditions stabilize. Source: World Cargo News

With decades of expertise in fixing and improving supply chains across Australia and the globe, I know what insights businesses need to stay proactive and ahead of disruption. Consider this your go-to resource for staying informed and making smarter logistics decisions. Get yours in your inbox - subscribe via LinkedIn or get in touch.

Be the first to know

No spam. Just the latest market news, tips, and interesting articles in your inbox.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.