Got a tracking number? Let’s see where your freight is

There has been a lot of talk recently about the new Wisetech price hikes and the uncertainty that it has created in the market. The changes to their pricing structure has caught their customers, and market in general, off guard with forwarders caught in the dilemma of on-forwarding the charges to their end customers directly (which in a lot of cases is the default setting) or eating the charges with the hope the price rise doesn't destroy their margins. The speed and opaqueness at which this has been rolled out is compounding the issue. Long story short, there are no good options for Wisetech’s customers. Wisetech has chosen to flex its muscles to the market and there is no looking back now. They will soon find out if their transition from a SaaS business model to an infrastructure business model charging a tax on the shipments they power, will work.

For Explorate customers there will be no “Cargo Automation Fee” appearing on your invoices all of a sudden. We do not rely on Cargowise for our billing or forwarding and transparency and predictability have been (and always will be) at our core. We are transparent with our pricing and for those using our SaaS features we will not be changing our pricing any time soon. We build great supply chains powered by data and trust. Unlike Explorate, Wisetech is certainly eroding that trust at an unprecedented rate which is a shame given its standing in the Australian market.

So to try and bring some clarity to the chaos that is occurring, if you are a shipper and your forwarder uses Cargowise (about 70% in Australia do) please reach out to them to find out if you will be impacted by the changes. Please be kind, this is a real cost for them.

If you are a forwarder, please reach out to me. I'm happy to help (while we don't build software for other forwarders to run as their core OS, we do help forwarders with how they can improve their customer experience) or be a shoulder to cry on. Sometimes those outside our industry don't know how much we have to lean on each other to keep freight moving.

Finally, if you are Cargowise (some Cargowise peeps do subscribe to our newsletter), please do better. Your customers have a hard job to do, please stop making it harder.

Conor Hagan, Co-Founder and Co-CEO at Explorate

The market’s found its footing… for now. Rates have steadied between USD 1000–1,700 per TEU across the CN-AU market.

Premium carriers are still holding higher, but with load factors strong and blank sailings tightening space, that calm could flip quickly once demand picks up mid-month.

Ports across Australia are feeling the usual end-of-year pressure. Weather, congestion and BMSB season are slowing operations, with more FCL containers being held for inspection and longer processing times across key terminals.

Wharf and road congestion are adding further delays, with containers taking longer to clear and move through the network. This can push out planned on-site dates and delivery windows during an already busy period.

To stay ahead, allow extra lead time, share critical delivery dates early and consider moving cargo sooner to avoid bottlenecks

Full container empty notification and collection: A reminder to allow 3 full business days (72 hours) for empty container collection. Please note that the day of notification will not be counted if the request is after 10am.

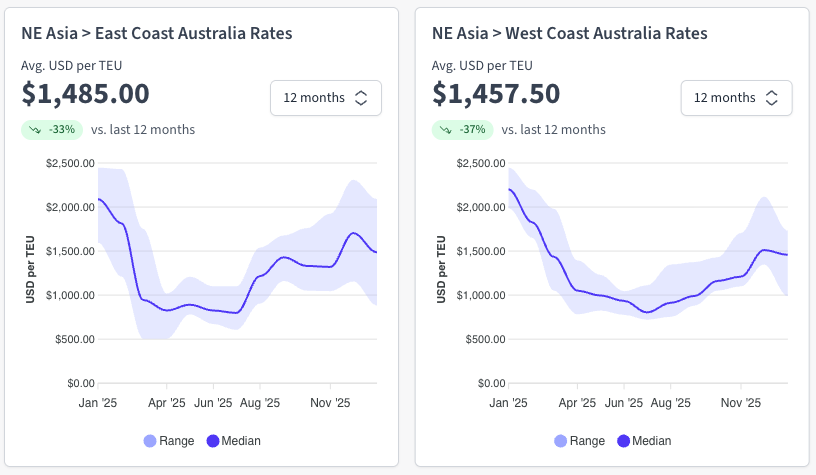

The NEA market has turned upward. Reduced capacity shifted the load mix, and bookings have started to rebound, prompting budget carriers to lift rates for the second half of December.

Even so, the market still sits softer than first expected, shaped by early-month overcorrections, thin inventories at key lines, and added forward capacity from certain carriers' new services in 2026.

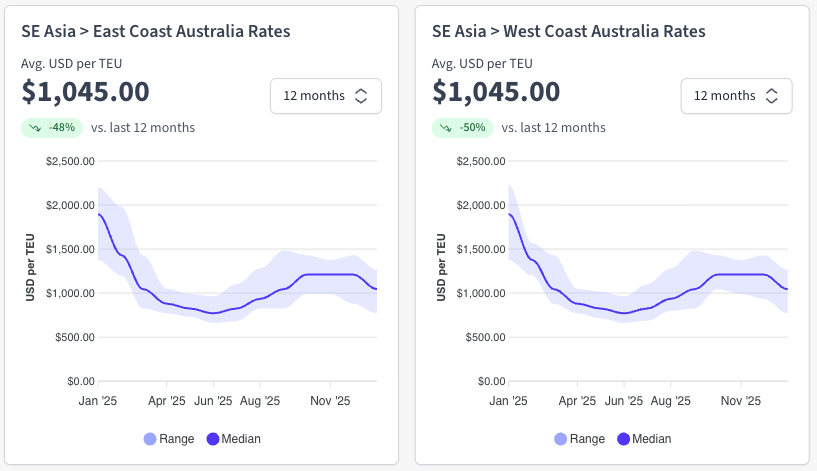

Rates across SE Asia remain steady into the second half of December. Export demand is still holding, but reliability is still under pressure mainly due to transhipment congestion.

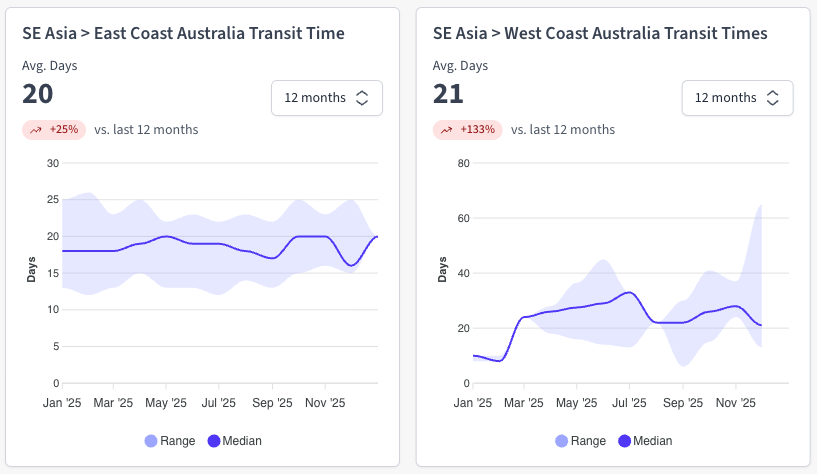

These conditions look set to persist through late December, so plan delivery timelines early where stock coverage is tight.

Rates across SE Asia remain steady into the second half of December. Export demand is still holding, but reliability is still under pressure mainly due to transhipment congestion.

These conditions look set to persist through late December, so plan delivery timelines early where stock coverage is tight.

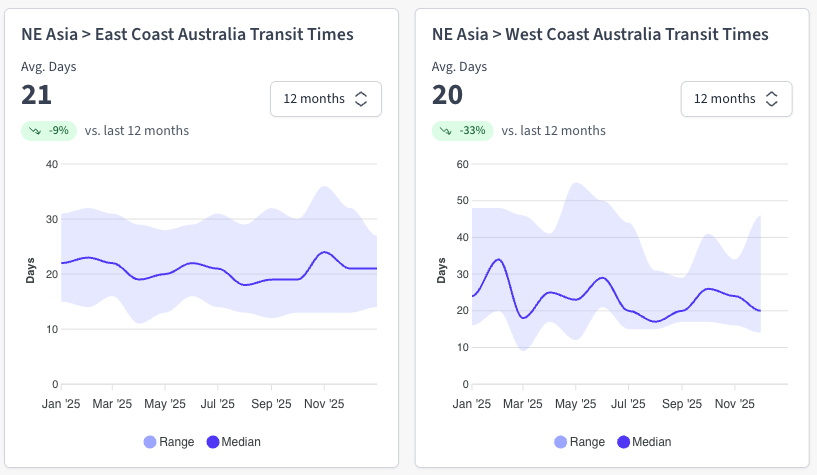

The Asia market is steady but tightening. NE Asia is lifting as capacity pulls back, and SE Asia is holding firm with some delays through key hubs.

With Chinese New Year on the horizon, we expect space to come under more pressure and rates to edge up through January

The US–China trade standoff continues to ripple through North American export markets, with retaliatory port fees briefly threatening to escalate costs before a one-year truce was inked on November 1. The pause has eased immediate pressure, but carriers are reassessing fleet deployment and exposure on both sides of the Pacific, which may influence capacity patterns through 2026.

The TPEB trade lane is cruising in calm waters right now; no fireworks, no freefall. Demand’s steady but uninspired, as shippers adopt a classic “wait-and-see” stance after the November tariff chatter fizzled out. It’s less “peak season rush,” more “holiday slowdown with a side of caution.”

Ocean freight rates across North America are holding steady, supported by stable demand and disciplined carrier capacity management. However, inland costs, including drayage and intermodal, are creeping upward due to limited trucking availability, driver shortages, and longer equipment turnaround times. Expect incremental rate adjustments through Q1 if inland congestion persists. Source: Maersk

It’s a tale of two networks - the ocean side is smooth, but the inland chain is fraying. The market is stable overall, yet the weakest link lies in post-arrival logistics, where shortages and delays are starting to add up. Shippers that rely heavily on rail or long-haul trucking should plan for longer dwell times and potential knock-on effects into early 2026.

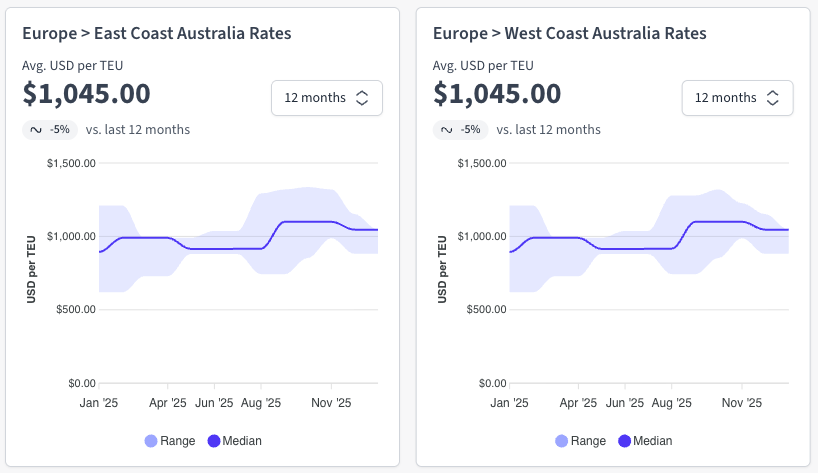

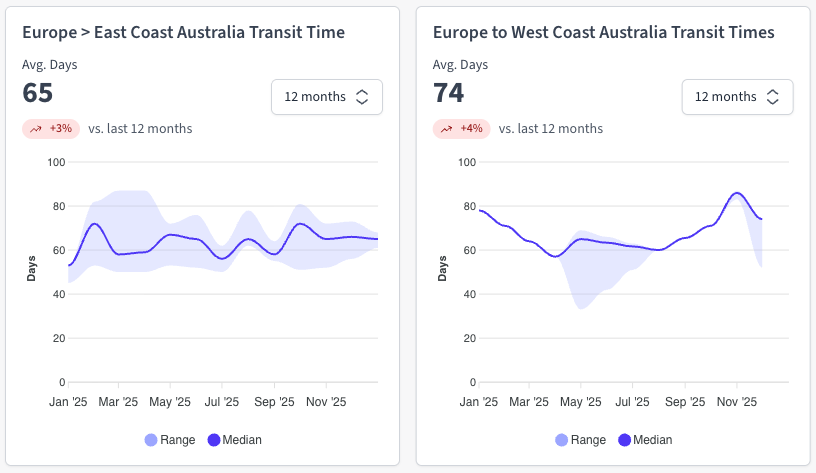

Whilst export rates out of Europe are holding fairly steady into the APAC region, congestion, dwell times, and equipment shortages still remain.

Transit times have remained fairly consistent, as delays continue through key transhipment hubs. The softer-than-anticipated peak season may help ease some of these delays going into early 2026.

Despite the last few weeks being consistent from both a rate and capacity side, other challenges are still prevalent.

From an AU import perspective transit times and securing space and equipment are still the key challenges. Hopefully congestion in Port Klang & Singapore will ease and with any luck we may see the Red Sea open up again in 2026.

Global air cargo rates are showing a subtle but steady lift heading into the year-end stretch. Spot rates from Asia Pacific to the U.S. climbed around 3% week-on-week to roughly USD 5.63/kg, driven mainly by stronger performance out of Hong Kong, Japan, South Korea, and Singapore - while China held flat. Despite the uptick in pricing, total export volumes out of Asia dipped about 2%, signaling that this mini rally is more about rate correction and yield recovery than a genuine demand surge. Southeast Asia and Taiwan continue to hold the strongest trade momentum, keeping the overall Asia-U.S. flow slightly ahead year-on-year.

The airfreight market ex-China to Australia is tightening slightly heading into December, with mixed space availability and mild upward pressure on select routes. While some carriers maintain stable rates, others are adjusting upward due to reduced frequency and limited lift - particularly from Shanghai (PVG) and Beijing (PEK) into Sydney, Melbourne, and Brisbane. Transit reliability remains uneven, with some carriers facing delays and added fees for palletized or bulky cargo.

The airfreight market is entering a mild “holiday hustle” phase - stable, not spectacular. Carriers are testing higher rate thresholds even as demand stays lukewarm, hinting at a market trying to rebalance yield before the traditional January slowdown. It’s not a boom, but it is a tightening, and late movers could find themselves paying more.

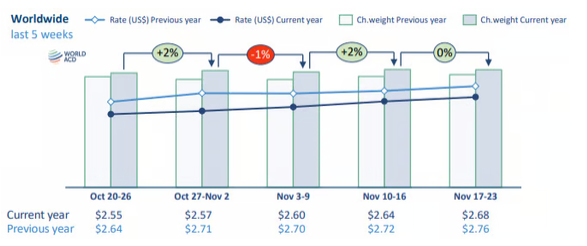

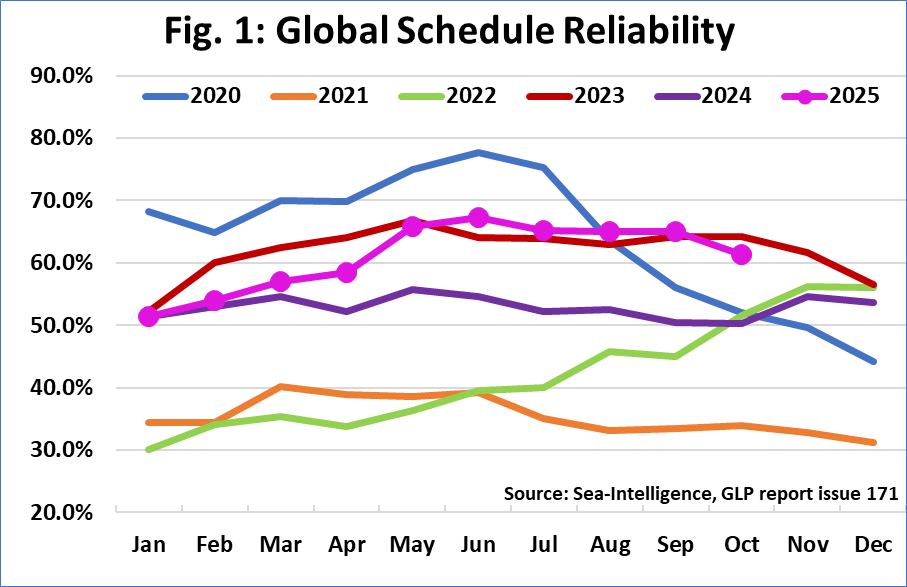

A small rate rebound and a slide in schedule reliability show a global market finding its feet but still sensitive to operational pressures.

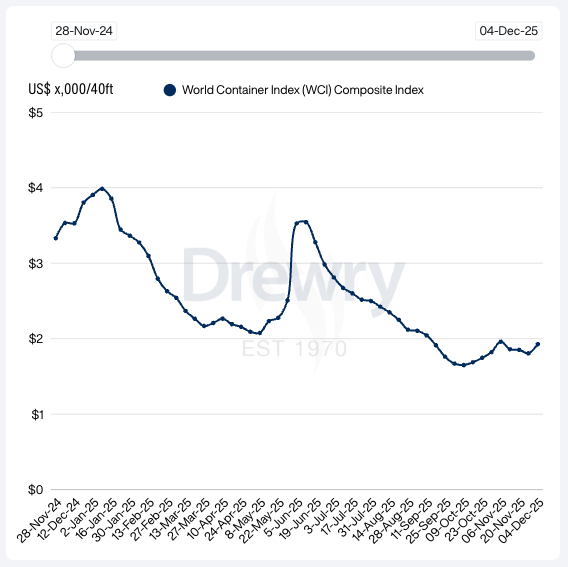

Global container rates lifted this week, with Drewry’s World Container Index rising 7 percent to USD 1,927 per 40ft container. It is a modest uptick, but enough to show the market edging out of its recent lull.

After three weeks of declines, the Transpacific finally saw some lift.

Carriers are leaning into weekly GRIs, using smaller, more frequent adjustments to maintain upward pressure on spot rates. Drewry expects rates to remain stable in the week ahead.

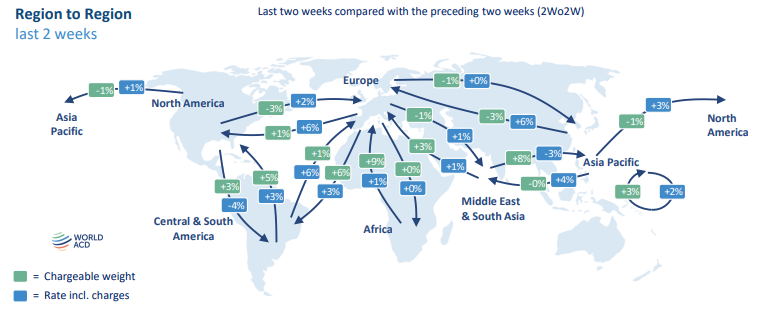

Asia–Europe continues its steadier run, supported by FAK increases ahead of contract talks.

Uncertainty around the Suez Canal continues to keep volatility high. A full return to the route would increase capacity and put downward pressure on rates, although any correction would likely be gradual as networks realign. Source: Drewry

Global schedule reliability slipped in October, falling 3.5 percentage points month-on-month to 61.4 percent. This is only the second significant decline of the year and follows three months of stability. Year-on-year performance remains positive, up 11.1 percentage points. Average delays for late vessel arrivals increased slightly to 4.98 days, still nearly a full day better than this time last year.

Maersk remained the most reliable carrier at 74.1 percent, followed by Hapag-Lloyd at 69.6 percent and MSC at 65.9 percent. Most others sat in the 50 to 60 percent range, with PIL the lowest at 44.9 percent. Source: Sea Intelligence

No spam. Just the latest market news, tips, and interesting articles in your inbox.