Got a tracking number? Let’s see where your freight is

Global shipping is under renewed strain as container freight rates continue to slide for the 13th consecutive week, driven by oversupply and weaker demand. Geopolitical tensions and changing tariff regimes, particularly between the U.S. and China, are adding further volatility to trade flows and routing decisions. At the same time, many companies are racing to strengthen supply chain resilience through technology, embracing AI, analytics, and automation, and shifting toward regional warehousing or nearshoring to minimise disruption risk. Cybersecurity has also emerged as a critical concern, with nearly one-third of supply chain leaders reporting recent cyberattacks on their networks.

Top three watch-points in the global supply chain for the coming month:

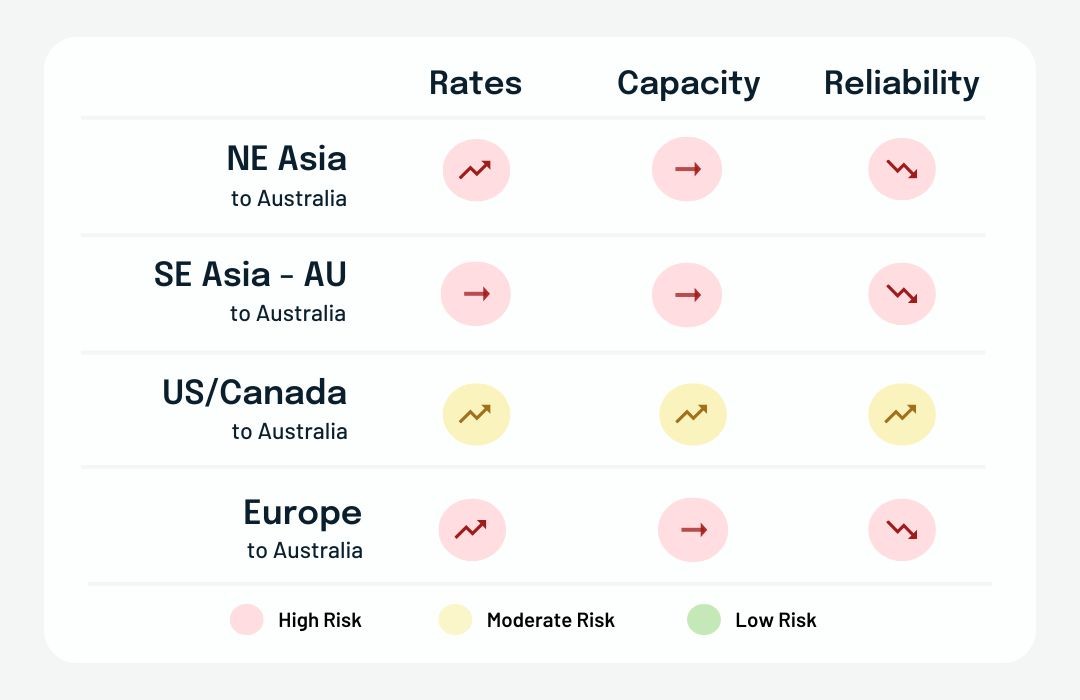

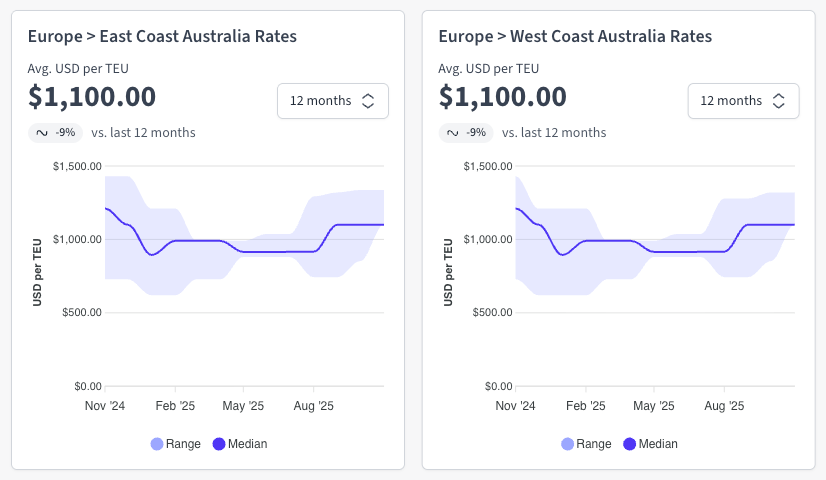

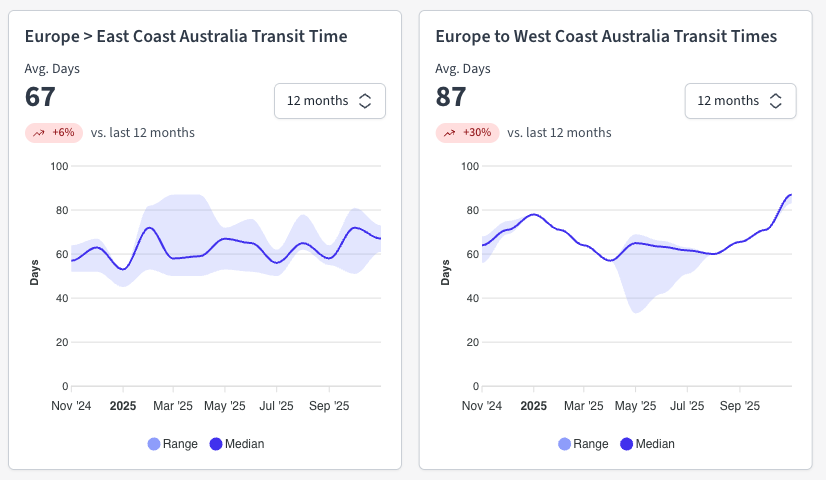

For Oceania importers, this means cheaper freight in the short term, but with volatility ahead as space tightens into year-end. Many are locking in rates early, diversifying supplier bases, and investing in tech-enabled supply chain tools to stay agile.

In short: Costs are down, risk is up - now’s the time to renegotiate, diversify, and digitise before the next market swing.

It’s been a relatively steady week across the major Australian ports, though a few hotspots are worth keeping on your radar.

In summary: conditions remain largely favourable for importers and exporters, but as we edge closer to the pre-Christmas surge, keeping an eye on vessel bunching and capacity adjustments will be key. Freight is flowing, for now, but the tide can turn quickly.

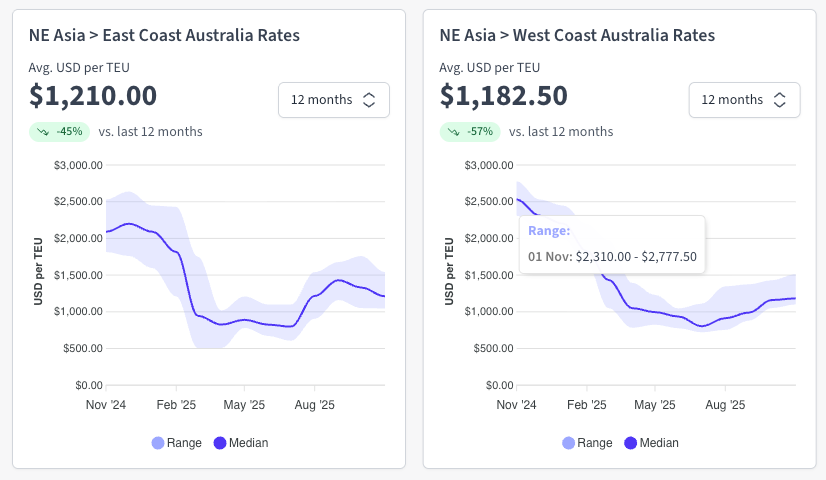

The China-Australia trade lane remains busy and resilient. Freight rates have firmed after an extended period of softness, with carriers largely aligned in their mid-October adjustments. MSC has adopted a more aggressive approach to fill recent extra-loader capacity, while premium carriers continue to hold firm, reflecting confidence in the strength of demand.

Multiple blank sailings and reduced extra loaders are tightening space availability through the second half of October. The pre-holiday cargo surge has overbooked vessels departing between 9–19 October, pushing new bookings toward the end of the month.

On the West Coast, Fremantle and Adelaide remain relatively stable, though congestion in Singapore has created some flow-on delays and higher utilisation across the network.

Southeast Asia is once again under weather pressure, with Tropical Storm Matmo marking the fourth typhoon in a month. Heavy rainfall exceeding 250mm is forecast across northern Vietnam, southern China, and the South China Sea, bringing flash flooding, high winds, and challenging sea conditions.

Operational impacts are most visible across Vietnamese ports, where vessel schedules are facing delays of up to several days. Cai Mep and Ho Chi Minh City remain congested as adverse weather slows quay operations and limits barge movements. Inland flooding is disrupting road transport to major manufacturing and export zones, creating flow-on effects at transshipment hubs like Singapore and Port Klang, where arrival bunching and high yard utilisation (85–95%) are adding pressure through mid-October.

Spot rates for the second half of October remain steady, but early indicators suggest a potential rate uptick from November as carriers recover lost productivity and reposition equipment.

The TPEB trade lane is entering a soft patch following the slowdown during Golden Week in Asia. Blank sailings across Weeks 41 and 42 are an intentional capacity control measure, reducing available space to approximately 62–69% of normal operations. Capacity is set to rebound to around 83% in Week 43, but this recovery is likely to create a short-term oversupply as demand remains low to flat.

Freight rates have continued to soften, prompting carriers to announce a General Rate Increase (GRI) effective October 15 in an effort to stabilise pricing. The next Shanghai Containerized Freight Index (SCFI) reading, due October 10, will provide clearer direction on market sentiment. Peak Season Surcharges (PSS) originally planned for mid-October have now been postponed to November 1, reflecting weak near-term demand.

The FEWB trade remains flat following the recent Golden Week holidays in China. To mitigate slow demand recovery, liners pre-loaded their roll pools before the break, overbooking by 20–50% to optimise utilisation in case post-holiday volumes failed to rebound, as seen in previous years.

Capacity management continues to be the main lever for stabilisation. The existing blank sailing program will maintain around a 10% capacity reduction in Weeks 42 and 43, followed by deeper cuts of –20% in Week 45 and –4% in Week 46. If booking momentum stays weak through late October, more cancellations are expected in November.

On the rate front, the Shanghai Containerized Freight Index (SCFI) remained unchanged during Golden Week and will next be updated on October 10. Carriers have announced General Rate Increases (GRIs) for the second half of October to prevent further deterioration, though market sentiment remains hesitant. A second GRI round and additional blank sailings are likely in early November if current efforts fail to gain traction.

Port congestion continues to weigh on operations across key North European gateways.

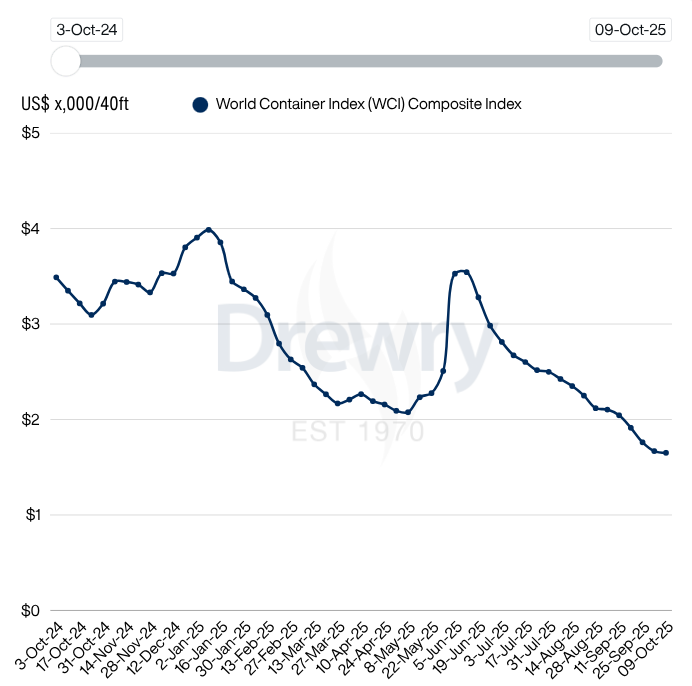

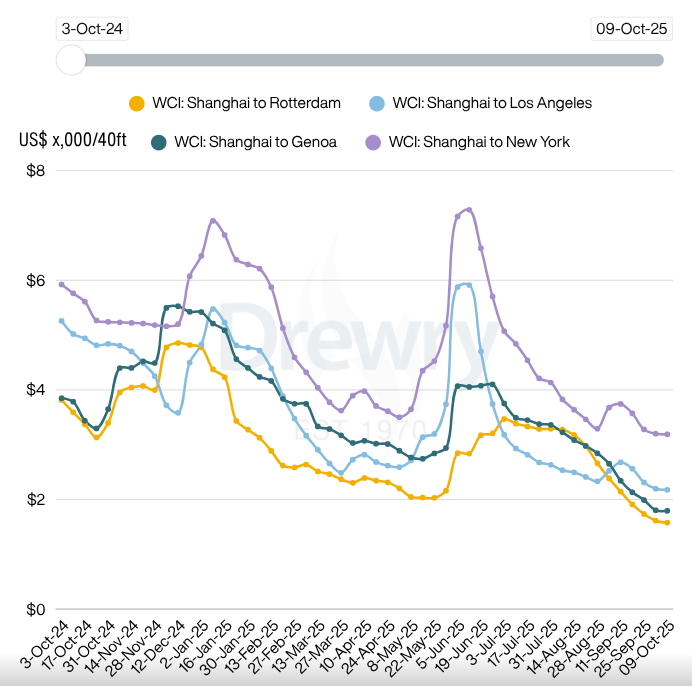

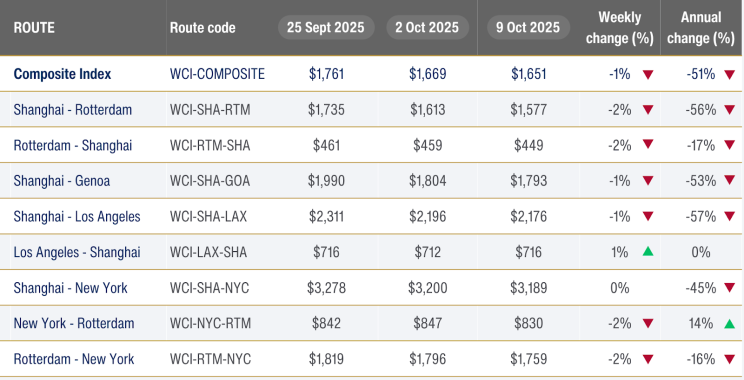

Drewry’s World Container Index fell 1% this week to USD 1,651 per 40-ft container, marking the 17th consecutive weekly decline and the lowest level since January 2024. On the Transpacific route, rates softened slightly, with Shanghai–Los Angeles dipping around 1% while Shanghai–New York held steady. Asia–Europe lanes remain under pressure, with further erosion across both Rotterdam and Genoa corridors. Drewry’s outlook suggests that as the supply–demand balance continues to weaken into Q4, spot rates are likely to contract further despite ongoing capacity controls. Source: Drewry

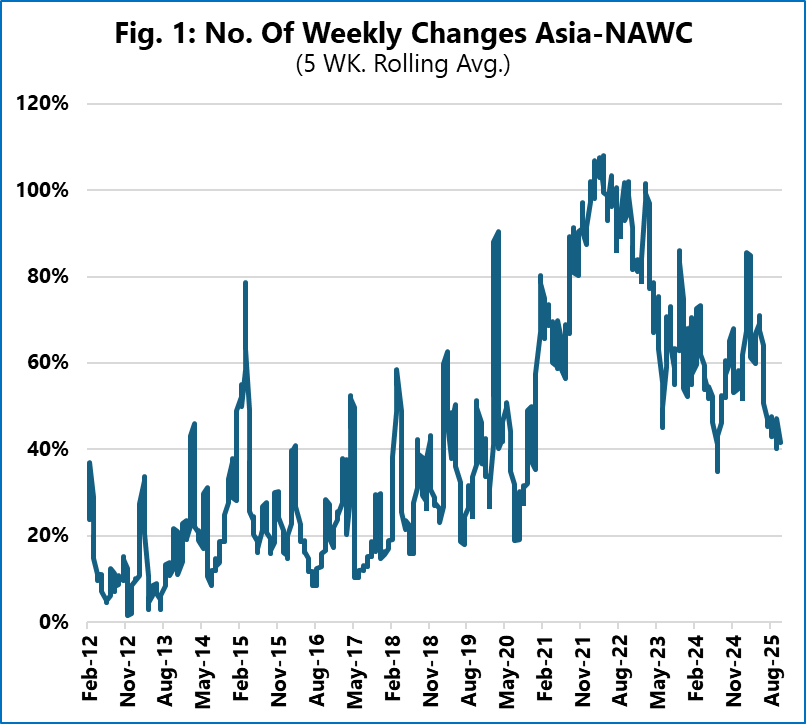

Sea-Intelligence reports that service instability in liner shipping has surged: the frequency of non-standard schedule changes (cancelled or extra sailings) across major trades in 2024–25 is now 2.5 to 3.5 times higher than pre-pandemic levels. On the Asia → North America West Coast trade, average instability now sits at 56%, up from ~23%. Similar structural shifts are seen across Asia → Europe, Asia → Mediterranean, and transatlantic routes. This signals a new normal of unpredictable weekly service changes that undermine schedule reliability and force shippers to absorb more disruption risk.

For Australian importers and exporters, softer global freight rates bring short-term cost relief, but rising schedule instability is the real risk. Frequent blank sailings, vessel delays, and transshipment congestion are creating unpredictable transit times, especially through Singapore and Port Klang. The market may be cheaper, but it’s also more volatile and operationally fragile.

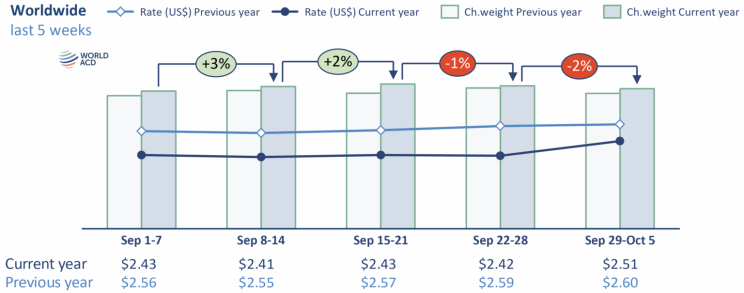

Tonnages from Hong Kong to Europe rebounded sharply: +29 % week-on-week after a storm-induced drop, while China → Europe also saw a modest lift of +6 %. Asia Pacific to USA volumes remain mixed - some markets dipped, others (Vietnam, Malaysia, Thailand) grew strongly. Overall, global rates are under pressure: Asia → USA spot rates are down ~18 % year-on-year, and Asia → Europe down ~11 %, despite rising volumes. Meanwhile, the global average full-market rate ticked up ~3 % WoW to USD 2.51/kg, but is still ~4 % below last year’s levels. Source: World ACD

We are thrilled to share that Explorate and Nick Scali have been named as finalists in the 2025 Australian Supply Chain & Logistics (ASCL) Awards for the Big Data, IT & Business Intelligence category! Our partnership has set a new standard for supply chain efficiency and resilience. We're incredibly proud of what we’ve achieved together and honoured to be named alongside influential companies like Freight Exchange, ADIONA and StarTrack Courier. This recognition highlights the incredible impact that data-driven technology and a collaborative approach can have on the future of global logistics. Learn more about the awards and see the full lists of finalists >>https://www.ascla.com.au/.

China’s exports surged 8.3% in September despite heavy tariff pressure, an acceleration largely powered by redirecting shipments from the U.S. toward Europe, ASEAN, Africa, and Latin America. Global demand is evolving: what used to flow through U.S. gateways is now increasingly routed through Southeast Asia, Mexico, and EU markets. This shift weakens the leverage of U.S. tariff strategy, signaling a deeper realignment in global trade networks. Beijing is reinforcing this pivot with infrastructure investments and trade deals to lock in new trading corridors. Source: Global Trade

U.S. Trade Representative Jamieson Greer says whether a sweeping 100% tariff on Chinese exports takes effect November 1 depends squarely on Beijing’s next move. Greer pressed China to roll back its expanded export controls, especially on rare earths, and warned that mixed messaging from Chinese officials is undermining any diplomatic path forward. Source: Reuters

A new hacking group dubbed the Coinbase Cartel has emerged with a clear focus on logistics firms, and DSV has already been targeted. They specialise in data exfiltration, staged leaks, and negotiated extortion - operating like a “professional” cybercrime syndicate rather than random attackers. Source: The Loadstar

Tens of thousands joined a national strike in Brussels as Belgium’s major unions protested government austerity and pension reforms. The walkout crippled air, port, and public transport operations, halting flights at Brussels and Charleroi airports and suspending vessel movements at Antwerp Port, where over 100 ships remain anchored offshore. Workers are opposing plans to raise the pension age and cut unemployment benefits, arguing the reforms unfairly target the middle and working class. The strike, largely peaceful but disruptive, has caused one of the most significant slowdowns in Belgium’s logistics network in recent years. Source: BBC

With decades of expertise in fixing and improving supply chains across Australia and the globe, I know what insights businesses need to stay proactive and ahead of disruption. Consider this your go-to resource for staying informed and making smarter logistics decisions. Get yours in your inbox - subscribe via LinkedIn or get in touch.

No spam. Just the latest market news, tips, and interesting articles in your inbox.