Got a tracking number? Let’s see where your freight is

The market is caught between weak global demand and aggressive capacity cuts. Typhoons have created major backlogs in South China, Golden Week is forcing a booking freeze, and carriers are preparing steep price hikes for mid-October.

Bottom line: The next 6-8 weeks will be challenging, testing the agility of APAC shippers.

China’s Golden Week holiday will run from Wednesday, October 1, to Wednesday, October 8. This year’s break is extended to eight days as National Day coincides with the Mid-Autumn Festival, driving one of the busiest travel and holiday periods of the year.

Takeaway: Importers and exporters should expect delays, congestion, and higher costs around this period. Advance planning, early bookings, and buffer time in supply chain schedules are essential to minimize disruption.

The first half of October is essentially an extension of late September trends. With Golden Week (Oct 1–8) overlapping Mid-Autumn Festival, new bookings are only being accepted for vessels with ETDs after 11–12 October.

South China Pressure Points (Shenzhen & Guangzhou): Trucking in South China has become particularly challenging due to:

Most Competitive Services Budget carriers have pushed rates down to USD 1100-1200 per TEU ex base ports (Shenzhen/Nansha/Ningbo/Shanghai). Qingdao pricing is slightly higher at USD 12000 – 1,250 per TEU due to stronger local demand. This is a clear rate war to capture market share ahead of the holiday.

Mid-Tier Services NEAX carriers and alliances like AUN are holding around USD 1150-1200 per TEU ex base ports and USD 1200-1300 per TEU ex Qingdao/Tianjin. These lines are heavily overbooking to build a strong roll pool through Golden Week.

Premium Services The A3 consortium adjusted rates down slightly but remains above the market average. Their current levels are USD 1400-1450 per TEU. Demand remains high for these services, and no further reductions are expected for now.

Australia West Coast Congestion at Singapore transshipment remains an issue, with rates currently ranging USD 1150–1200 per TEU depending on the carrier.

📌 Market Outlook: Pre-Golden Week promotions and extra-loader deployments have created a short-term buyer’s market. Rates remain under pressure through early October, but with extensive blank sailings planned and the seasonal cargo rush resuming post-holiday, substantial increases are expected from mid-October onward.

ANL: USD300.00 per TEU GRI for all cargo from North East Asia, South East Asia, Indian Sub-Continent & Middle East to Australia and New Zealand. Effective from the 15th October.

MSC: USD300.00 per TEU GRI for all cargo from China, Hong Kong, Taiwan, Japan, Korea, Cambodia, Thailand, Vietnam, Malaysia, Myanmar, Singapore, Philippines, and Indonesia to Australia and New Zealand. Effective from the 15th October.

OOCL: USD300.00 per TEU GRI for all cargo from North East Asia to Australia. Effective from the 15th October.

OOCL: USD300.00 per TEU GRI for all cargo from North & South East Asia to NZ. Effective from the 15th October. Southeast Asia Rates

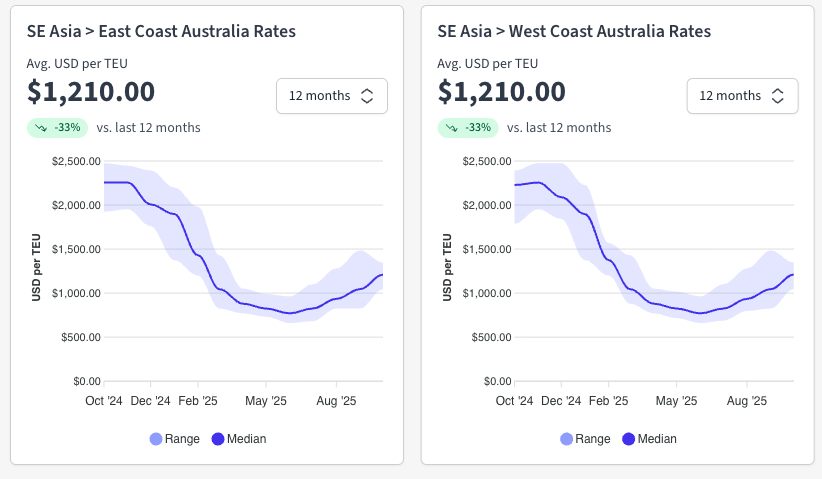

Rates vary between USD1000-1300 per TEU for the majority of ports into both the East & West Coasts of Australia.

Additional Loaders:

PIL: TS BANGKOK 2516S / 1787 TEU

SHK 22/Oct →HKG 23/Oct→NSA 24/Oct→BNE 5/Nov→SYD 8/Nov→MEL11/Nov

ANL: CMA CGM SEMARANG / 2700 TEU

TAO 27/Oct→SHA 29/Oct→SHK 2/Nov→SYD 15/Nov →MEL 18/Nov

Week 41

A3: OOCL KUALA LUMPUR V.184S - delayed by 8 days

NEAX: WIDE JULIET V.0115S - advanced by 6 days

PANDA/ZAX: Blank Sailing

WALLABY: MSC NASSAU IV KN541A - delayed by 2 days

CAT: TIAN SHUN HE V.2506s - delayed by 2 days

CA2: KOTA LIHAT V.0217s - delayed by 5 days

Week 42

CAT: Blank Sailing

DRAGON: Blank Sailing

CA2: KOTA LAWA V.0099s - delayed by 5 days

Week 43

WALLABY: Slide 1 week

Week 49

CAT: Blank Sailing

South China Super Typhoon Ragasa brought operations to a standstill across key terminals - Yantian, Shekou, Nansha, and Hong Kong - with gate and rail services suspended between 22 and 25 September. While activity officially resumed on the 25th, backlogs are still unwinding with delays averaging 4–5 days. Adding to the weather chaos, Tropical Cyclone Bualoi intensified on 25 September and is tracking towards the Philippines, Vietnam, Laos, and China, with potential for further disruption this week.

Vietnam Congestion continues to weigh heavily on Vietnam’s major gateways. At Haiphong, vessel waiting times are hovering at 1 day, with yard utilisation pushing 80%. Meanwhile, Ho Chi Minh City is facing even tighter pressure, with average waits stretching beyond 2 days and Cat Lai’s yard running at 90% utilisation.

Malaysia At Port Klang, berth congestion and vessel bunching have pushed average waiting times to just over 1 day. Yard density sits at 85%, restricting overall productivity and slowing container movements.

New Zealand High winds knocked out 57 hours of operations at Tauranga’s TCT last week, with intermittent weather impacts continuing into mid-September. While services have resumed, the stop-start conditions are straining schedule reliability.

Sri Lanka Colombo is under pressure, with terminal operations slowed by heavy yard congestion, rising transhipment volumes, and ongoing weather disruptions. Productivity remains constrained across key terminals.

Chittagong: Average vessel waiting times are currently around 1.35 days. Berthing congestion has eased slightly, but delays of 1–3 days persist. Yard occupancy is running high at 85%, with equipment breakdowns and wider logistical challenges hampering smooth operations.

Dhaka ICD: Inland congestion is acute, with dwelling times exceeding 20 days due to locomotive shortages. Overweight containers face even longer delays of more than 30 days, while train departures remain restricted, adding to the inland supply chain strain.

AUSTRALIA: Labour Day: 6th October (ACT, NSW, SA), King’s Birthday: 6th October (QLD)

SINGAPORE: Deepavali: 12th November

MALAYSIA: Deepavali: 12th November

TPEB: Peak Season Surcharge (PSS): Deferred until Oct 15 - no surcharge applied pre-Golden Week. The Sept 15 GRI has been fully withdrawn. Carriers are lowering rates to stimulate demand, with many extending September levels through Oct 14.

Importers pulling shipments forward ahead of potential tariffs created a softer-than-expected peak season. The result: oversupply in the market, weaker demand, and a quiet lead-up to Golden Week.

Carriers are managing excess capacity with blank sailings to prevent rates from sliding further. For example, the Premier Alliance has suspended its PS5 service from China to the U.S. West Coast.

Both the East and West Coast markets remain oversupplied, with no noticeable pre-Golden Week rush. Space remains widely available, particularly to the East Coast.

Operations at the Port of Long Beach were impacted by the ZIM Mississippi container incident. Discharge resumed on Sept 17 (U.S. local time), but all containers linked to the incident remain on hold pending a U.S. Coast Guard investigation. Impacted cargo owners will be updated once the release is confirmed.

Trump’s proposed 100% tariff on non-U.S. films Donald Trump has doubled down on a threat to impose a sweeping tariff on films produced outside the U.S., sparking alarm across the global screen industry.

👉 For the full update, read our blog: U.S. Tariffs and Policy Changes: What They Mean for Global Supply Chains

FEWB: The Sept 15 GRI was fully withdrawn due to lack of demand. Carriers have responded by lowering rates to capture bookings, with many extending current levels through Oct 14.

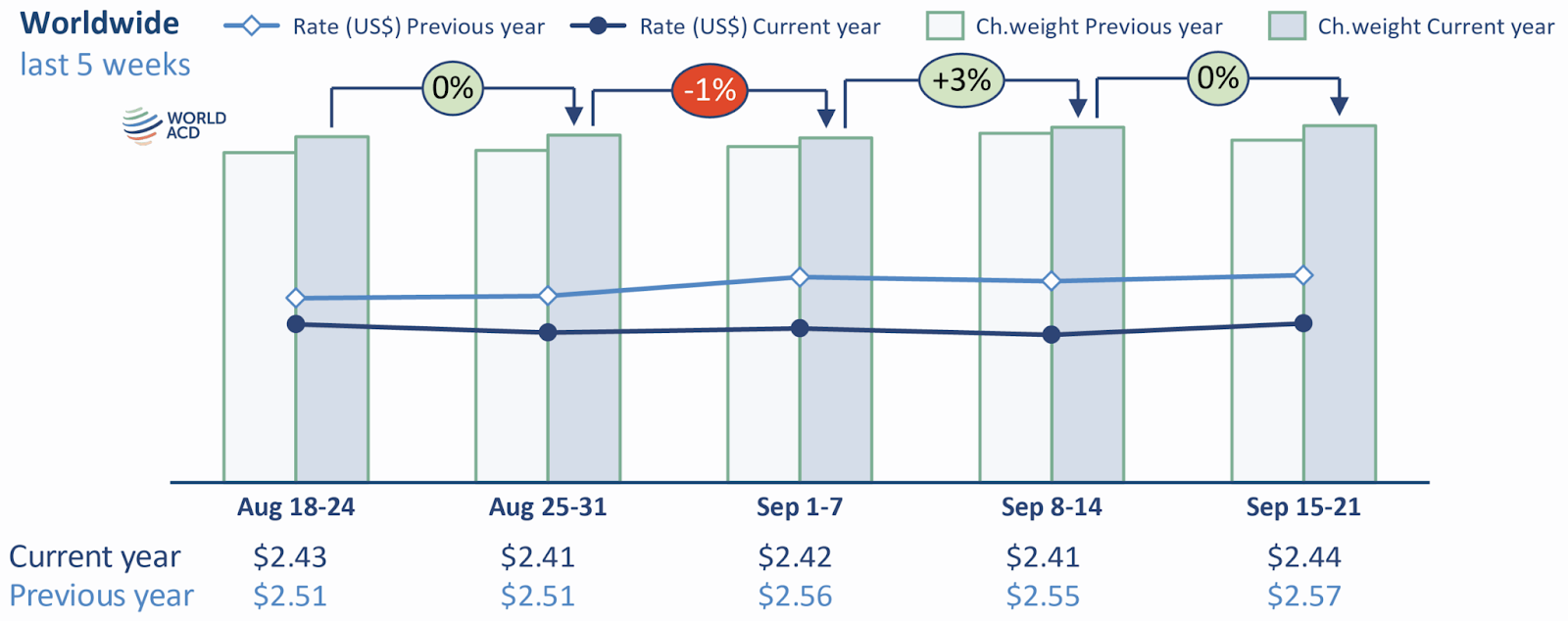

TAWB: Spot rates from North Europe → U.S. East Coast are averaging USD 1,838–1,911 per 40’ (mid-September, Xeneta). This represents a ~5% decline since June and a ~25% drop compared to January 2025.

FEWB: Around 25% of capacity will be blanked in Weeks 40–41, though this is a smaller withdrawal than in previous years, meaning overall supply remains adequate through late September into early October.

Congestion at European ports has eased, but demand remains weak as retailers continue to manage high inventory levels and exercise caution due to inflationary pressures.

TAWB: Equipment shortages remain an issue in inland and regional markets - particularly Austria, Slovakia, Hungary, Southern/Eastern Germany, and Portugal.

FEWB: Service disruptions are limited, and with congestion easing, reliability is relatively stable compared to earlier in the year.

Spain Valencia continues to feel the pinch from vessel bunching, with average waits close to 3 days. Yard density sits high at 80% with mild gate congestion.

Italy National protests on 22 September disrupted port access across the country. Gioia Tauro is reporting 3-day vessel waits, while La Spezia is averaging 2.5 days with yard density at 77% but still manageable.

France Labour unions have announced a 24-hour strike on 2 October, expected to cause disruption nationwide. Fos-sur-Mer currently has average vessel waits of around 2 days.

United Kingdom London Gateway remains relatively balanced - yard utilisation at 60% for dry and 50% for reefers. High winds earlier this week forced pilot station closures, but vessel ops continued. Berth 4 remains draft-restricted to 15.1m. Rail terminal performance has picked up following the resolution of RMG failures.

Belgium Antwerp is tight, with vessel waits just over 1 day. Yard utilisation is 75–80%, reefers near 95%, and berths are full. Strong winds closed pilot stations and delayed Gemini rotations. Barge congestion triggered the opening of an additional terminal to relieve the backlog.

Netherlands Rotterdam is averaging 1.5-day vessel waits. Yard utilisation at ECT stands at 85%. Gang availability remains limited. Barge/feeder delays stretch to 48 hours, ITT moves are restricted, and berthing is full.

Germany Hamburg: 2-day average vessel waits, with HHLA terminals impacted by staff assemblies and strong winds. CTA productivity was reduced by an IT failure early in the week (now resolved), but construction still restricts berth capacity. CTB is congested, with waits up to 7 days despite yard density holding steady at 75%. Bremerhaven: Rail links between Bremen and Lübberstedt will be suspended 2–6 October, with diversions via Bremervörde and Cuxhaven.

Poland Gdynia’s average vessel wait stands at 3 days.

GreecePiraeus remains one of the worst congested ports in the region, with vessels waiting almost 5 days on average.

EU: The Drewry World Container Index fell by 8% this week to USD 1,761 per 40ft. On the Asia–Europe corridor, Shanghai to Rotterdam rates dropped around 9% to USD 1,735 per 40ft, while Shanghai to Genoa fell by roughly 7% to USD 1,990 per 40ft. Carriers are actively trimming capacity on these routes in an effort to counter weakening demand ahead of China’s Golden Week factory closures. Drewry forecasts that the supply-demand balance will continue to loosen over the coming quarters, which could drive further spot rate declines.

US: On the Transpacific, Shanghai to Los Angeles spot rates fell by about 10% to USD 2,311 per 40ft, while Shanghai to New York rates dropped around 8% to USD 3,278 per 40ft. These decreases follow several weeks of earlier rate gains driven by General Rate Increases and blank sailings, which have now lost momentum. Overall, the trend in US-bound rates reflects weak demand and a broader easing of upward pricing pressure across the market.

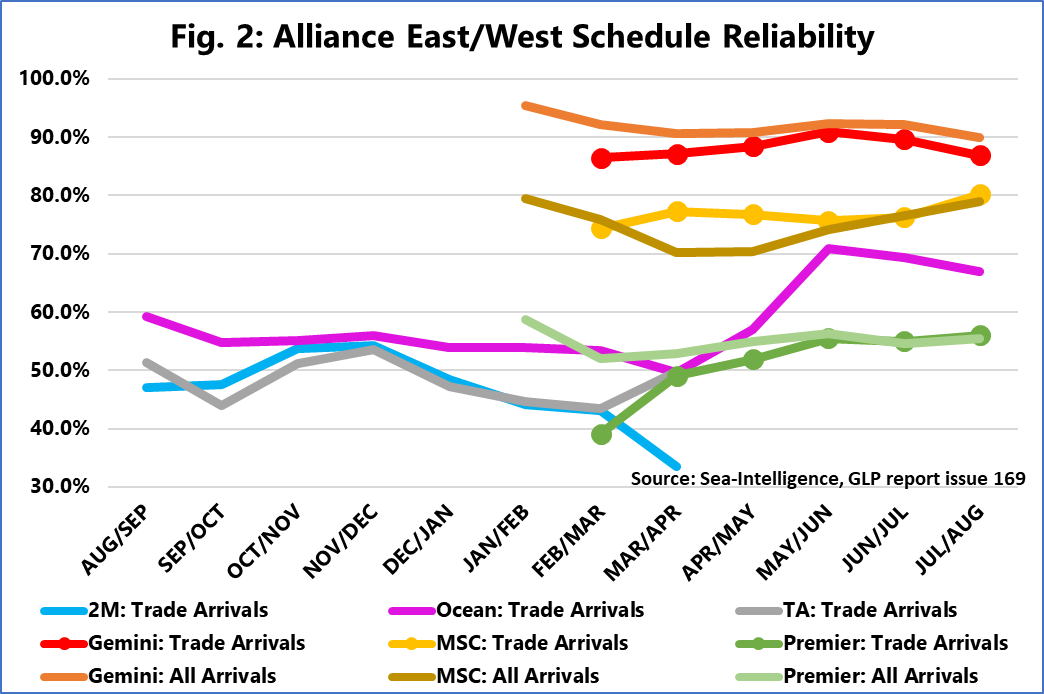

Global liner schedule reliability has stabilized in the range of 65–68 % since May 2025, with May hitting 65.8 %, the highest level since November 2023. Reliability saw a sharp month-on-month jump of +7.4 percentage points in May, and a year-on-year gain of ~10 points. Among top carriers, Maersk led with ~75.9 % reliability, followed by Hapag-Lloyd. The lowest performer among the top 13 was ONE, at ~55.1 %. Sea-Intelligence also introduced a dual-metric approach - “all arrivals” vs “trade arrivals” - to better assess performance across the newly formed alliances, which will be fully evaluated once alliance transitions are complete.

Source: Sea Intelligence

Maersk was the most reliable top-13 carrier with schedule reliability of 76.4%, followed by Hapag-Lloyd with 72.4%. The next 6 carriers were in the 60%-70% range, with the remaining carriers in the 50%-60% range. Wan Hai had the lowest August 2025 reliability of 53.3%.

Shipping lines have sharply increased blank sailings ahead of Golden Week, withdrawing an additional ~544,000 TEU over the past four weeks across Transpacific and Asia-Europe trades. Some alliances moved early: the Premier Alliance led from week 32, with Ocean Alliance following cautiously, then accelerating in week 37. MSC and Gemini were slower to act - Gemini used a single mass withdrawal, while MSC accelerated aggressively in week 36. Despite the timing differences, the end result is that capacity reductions on these routes are now roughly in line with historical holiday levels.

Source: Sea Intelligence

Rates and Pricing Trends Global average air cargo rates rose slightly, up around 1% week-on-week to USD 2.44/kg. While this reflects some stability in demand, rates remain ~5% below last year’s levels. The biggest pressure point continues to be the Asia–U.S. trade lane, where spot rates are nearly 20% lower year-on-year. Taiwan stands out as an exception, recording an 11% YoY increase on the back of strong semiconductor and electronics exports.

Asia–Europe Developments Volumes on the Asia–Europe corridor grew by roughly 6% YoY, showing resilience despite broader market weakness. Spot rates remain below 2024 levels across most origins, though China has turned positive again with a 3% increase in week 38 — signalling early signs of recovery ahead of the Golden Week holiday period.

Operational Disruptions The impact of Super Typhoon Ragasa continues to be felt, particularly across South and East China and Hong Kong, where flight cancellations and capacity constraints have tightened supply. With Golden Week approaching, forwarders are already reporting stronger spot rate activity out of China, pointing to further volatility in week 39.

Outlook The market remains in a delicate position: global demand is steady but uneven, pricing under pressure, and seasonal disruptions (typhoon recovery + Golden Week factory closures) are likely to drive short-term volatility. Rates are expected to firm temporarily through early October as China’s export push resumes after the holiday.

Source: World ACD

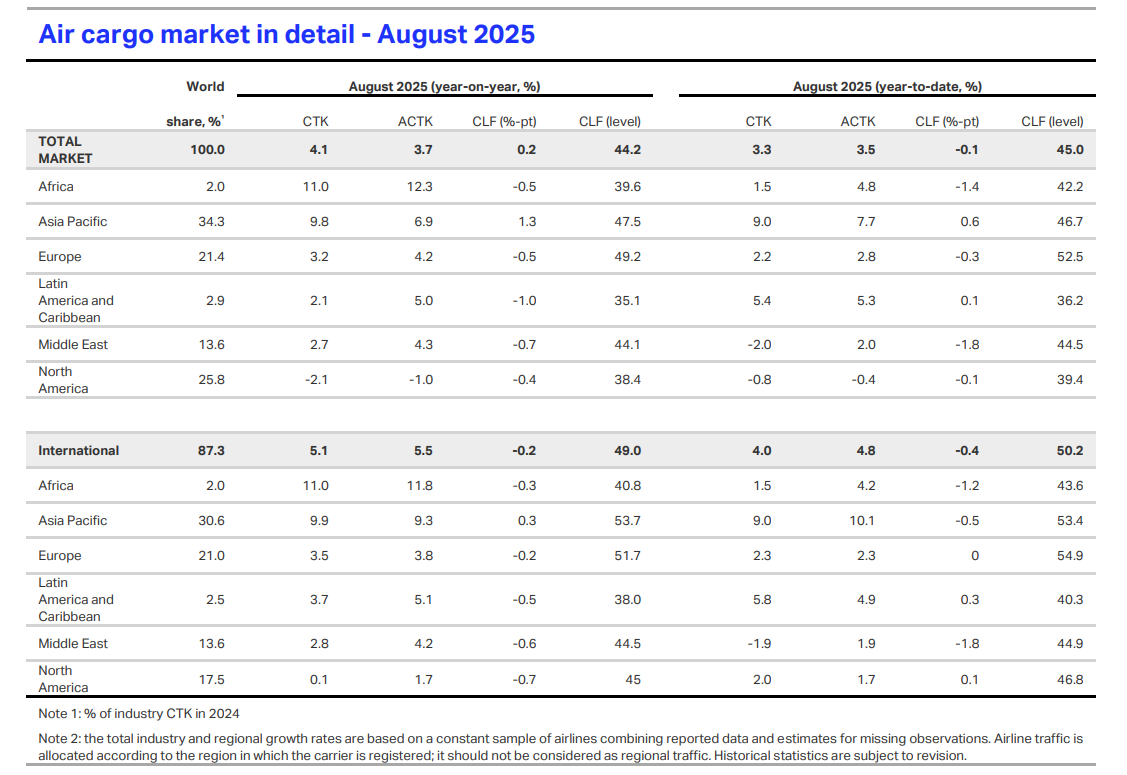

The air cargo market held up reasonably well in August, though some cracks are showing. Overall demand (measured in cargo tonne-kilometers, CTK) rose 4.1% year-on-year, down from July’s 5.5% growth. International routes saw 5.1% YoY growth, with Africa (+11%) and Asia-Pacific (~9.8%) leading the way. Capacity (available tonnage) also expanded (~3.7% YoY), so load factors ticked up only modestly. Fuel prices helped - jet fuel dropped ~6.4% YoY - but yields (freight rates per kg) continued to soften ~2.0% YoY, even with a slight month-on-month increase.

Source: IATA

Some regions are under pressure: North American carriers recorded a 2.1% drop in demand, and cargo yields are under stress globally. Belly capacity (freight on passenger aircraft) is still growing strongly, now making up over 56% of freight tonnage, while dedicated freighters are present but under more strain. Trade rerouting is also notable: high-tariff pressure has shifted some Asian exports away from North America toward Europe, Africa, and intra-Asia corridors.

China has announced plans to amend its international maritime transport regulations in direct response to the USTR’s proposed port fees targeting Chinese-built vessels and carriers. The move signals a clear tit-for-tat approach, giving Beijing the authority to impose reciprocal measures against any country that enacts protectionist charges or restrictions on Chinese shipping operators. This development highlights the escalating trade tensions between the U.S. and China, with potential implications for global shipping costs and supply chain stability.

Source: The Loadstar

Typhoon Bualoi made landfall in northern central Vietnam on September 29, causing severe damage and widespread disruption. At least 13 people have died, with 17 missing. Strong winds and heavy rainfall damaged homes, roads, and bridges, while over 347,000 households lost power. Flooding inundated streets and cut off Highland communities, and four coastal airports in central Vietnam were shut down, triggering flight cancellations and delays. The storm intensified rapidly, generating waves up to 8 meters, and then weakened as it moved inland toward Laos.

Source: ABC News

With decades of expertise in fixing and improving supply chains across Australia and the globe, I know what insights businesses need to stay proactive and ahead of disruption. Consider this your go-to resource for staying informed and making smarter logistics decisions. Get yours in your inbox - subscribe via LinkedIn or get in touch.

No spam. Just the latest market news, tips, and interesting articles in your inbox.