We have now entered full peak-season mode; space is tight, rates are firming, and reliability is being strained by weather delays, transhipment congestion, and carrier capacity controls. Singapore and North Asia feeder hubs are acting as chokepoints, pushing roll risk higher on cheaper services, while premium and mid-tier sailings are filling out weeks in advance. With November departures aligning to pre-Christmas and pre-CNY arrivals, this is now a book-early-or-miss-the-window market where uplift certainty matters more than rate hunting.

For Oceania importers, the message is clear. Space is now the constraint, not price. Book early and align service tier to urgency or risk missing pre-Christmas and pre-CNY delivery windows.

Regional Market Trends

Adverse weather across Southern states causing intermittent Empty Park closures due to high winds. Expect this to continue over the coming month with potential delays expected.

Sydney (SYD):

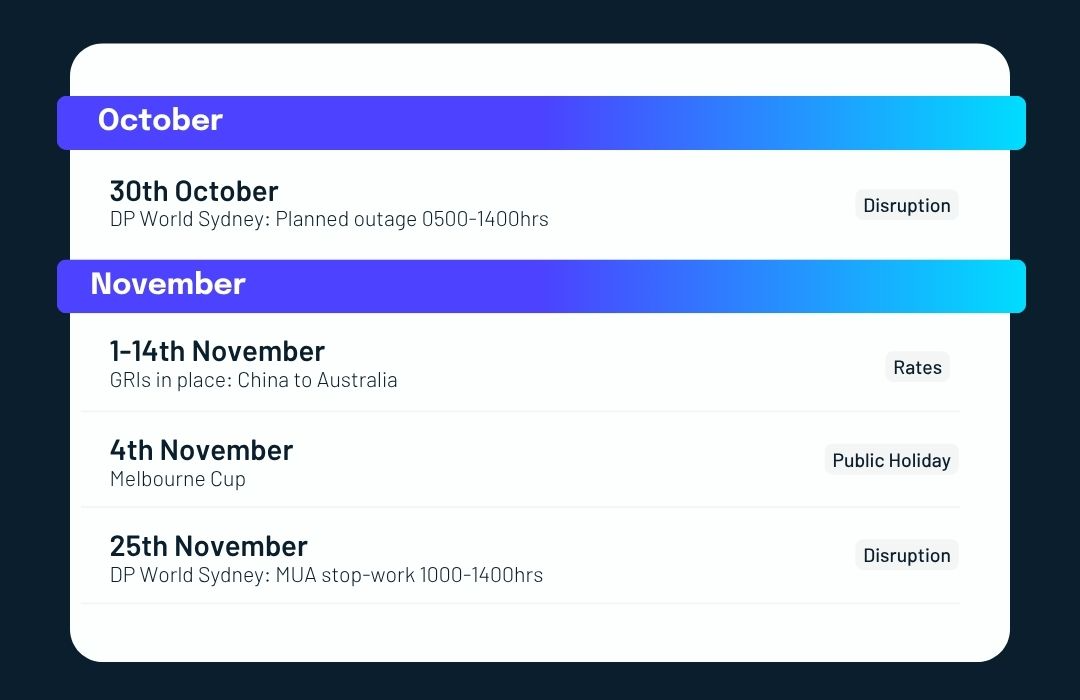

Remains the most operationally volatile east coast port at present, with high winds and vessel bunching already slowing quay productivity and increasing omission risk. DP World Port Botany has scheduled a planned outage on 30th October. This may cause some delays to deliveries.

Volatility will be compounded by an MUA-authorised stop-work meeting at DP World Sydney on Tuesday 25 November from 10:00am–02:00pm, during which all terminal operations will cease. Expect flow-on delays to receival/delivery slots that afternoon and into the following 24–48 hours as the terminal clears backlog.

Brisbane (BNE)

Brisbane remains comparatively stable, but vessel bunching and the broader peak-season squeeze are creating intermittent yard pressure. Operations continue without major weather disruption, though some terminals are edging toward capacity during peak call windows, increasing the risk of short-notice delays. Slotting and receival windows remain functional, but bookings are filling quickly, and schedule recovery tactics upstream (China) are flowing through in the form of tighter turnaround times.

Melbourne (MEL)

Melbourne is experiencing a compounding set of constraints: strong winds last week slowed operations, landside traffic through the wharf precinct has been periodically restricted, and the Melbourne Cup public holiday has reduced labour availability. These factors have reinforced existing congestion - yard density is elevated, with longer truck turnarounds and increased rollover risk for late-cutoff cargo. Carriers are prioritising schedule recovery over call flexibility, which will remain visible for the next 1–2 weeks.

Fremantle (FRE)

Fremantle continues to feel the flow-on effects of east-coast congestion and service rotation changes, with omission risk higher than usual. While weather conditions have been stable, available berthing windows are tight, and carriers are actively managing capacity by skipping or truncating AUWC calls to maintain network timing. Arrival reliability is materially weaker than pre-peak levels, particularly for sailings cascading from Singapore, where congestion remains a binding constraint.

Adelaide (ADL)

Adelaide remains the most stable touchpoint in the national network, with no major weather events or disruptions over the past week; however, on-time performance is still lagging due to upstream issues rather than terminal inefficiency. The port is absorbing diverted cargo from omitted west-coast calls at times, which can briefly pressure yard capacity. That said, risk remains lower here than in SYD/MEL - delays are more predictable and driven by schedule recovery rather than local bottlenecks.

Other Local News:

Reefer equipment and 20ft availability remain tight across most terminals, so early equipment pickup is essential - shippers should be prepared to pivot to 40ft or LCL where required.

Port schedule reliability into Australia continues to trail global averages, with delays of around 4–8 days depending on lane and rotation change impacts.

In New Zealand, recent KiwiRail maintenance works around Auckland/Tauranga have reduced trans-Tasman efficiency, with road bridging slower than rail and some minor flow-on to AU arrivals. Regionally, a frequency uplift on the WPAC service from late October/November should marginally improve connectivity into the Pacific and East Coast Australia. There are also small windows of opportunistic uplift into Townsville, where ad-hoc direct China calls are being trialled, but these should be treated as tactical rather than a reliable base routing

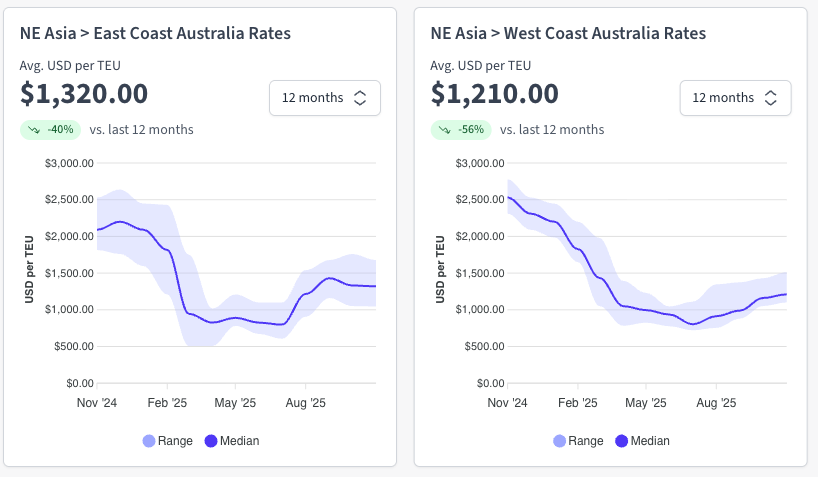

North East Asia: Market Overview

The China–Australia market has entered a fully fledged peak-season surge, with pricing momentum in late October spilling aggressively into November. The confluence of pre-Christmas volume, tariff-driven front-loading out of China, and limited redeployment of tonnage from the US trade has turned an already hot market into a capacity squeeze.

Carriers have successfully pushed through a full GRI, widening the spread between service tiers and reinforcing aggressive pricing behaviour for sailings departing 1–14 November. Additional loaders have helped dampen what could have been even higher benchmarks, but these are quickly absorbed and concentrated in the first half of the month. Barring a late November cool-down, the current levels are likely the market peak for 2025 - elevated, but controlled compared with last year’s volatility.

Ocean Freight Rates

Rate levels for the first half of November have now clearly levelled into three pricing bands, reflecting both service quality and booking pressure.

Budget services are sitting around USD 1,600–1,700 per TEU, driven by cost-sensitive liftings and additional loader capacity that still needs to be filled.

The mid-tier bracket has firmed at roughly USD 1,750–1,800 per TEU, reflecting faster transit times and higher schedule reliability, with stronger demand locking in these increases after the GRI.

At the top end, premium services have moved decisively to USD 1,950 per TEU, where pricing is less about market matching and more about guaranteed uplift and roll protection.

This widening spread between tiers signals not just a capacity squeeze but also active carrier yield management: space is being allocated according to willingness to pay, and rate discipline is being maintained to preserve peak-season margins.

Capacity and Schedule Reliability

Space conditions have tightened materially across the lane, with vessel departures from China now facing delays linked to ex-Typhoon Fengshen, compounding an already overbooked environment.

Widespread rollovers continue as vessels sail above allocation, while carriers are actively deploying port omissions and rotation changes to protect their schedules - with the Australia East Coast maintaining priority and Australia Freemantle (AUFRE) the most consistently impacted by skipped calls.

Congestion in Singapore remains a key bottleneck and is severely restricting transshipment fluidity, further reducing effective capacity on both east and west coast routings. Over the next 3–4 weeks, the market is expected to remain extremely challenging on space, with what is now being considered the “true” peak-season window, as sailings in this period are the ones intended to arrive into Australia just ahead of Christmas and Chinese New Year inventory cut-offs.

Airfreight rates have also begun climbing in parallel, with space tightening quickly; time-sensitive SKUs now require earlier service selection and booking discipline to ensure on-site delivery dates are met.

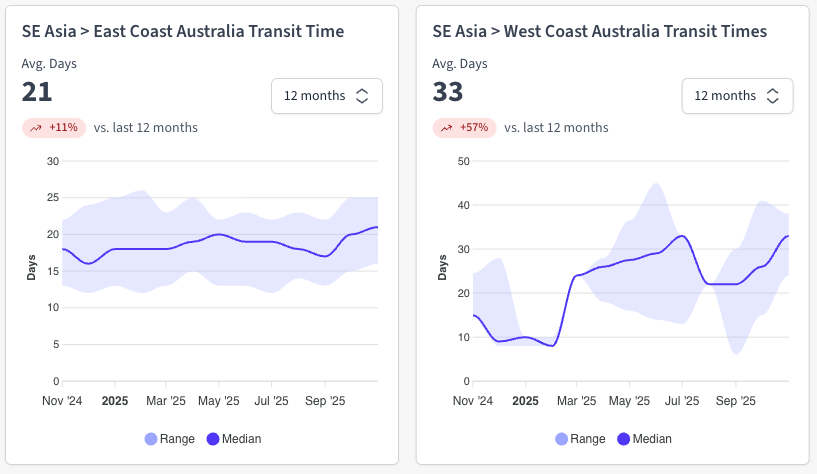

Southeast Asia: Market Overview

Southeast Asia is now firmly in peak-season conditions, with space tightening, rates rising, and congestion across key hubs like Singapore, Port Klang, and Vietnam. Laem Chabang remains a major bottleneck, and lingering weather impacts from ex-Typhoon Fengshen are adding schedule risk. The next 3–4 weeks will be the tightest as sailings target pre-Christmas and pre-CNY arrivals into Australia. Equipment is constrained, especially reefers and 20s, and airfreight is also firming as urgent cargo shifts off the water.

Ocean Freight Rates

Rates ex-Southeast Asia are firming into early November, with most origins posting moderate to double-digit increases in the 1–14 Nov window. Taiwan and Vietnam show some of the steeper uplifts (+16%), while Malaysia shows +11% increases. Singapore and Jakarta are also rising, though at a steadier pace (+5% range), reflecting stable but tightening liftings. Thailand sits in the middle bracket with a gentle upward push.

The key theme across the region is consistent: rate increases are broad-based rather than isolated, signalling a structural move into peak-season pricing, with carriers actively managing space and pushing early-month GRI momentum before pre-Christmas and pre-CNY cargo ramps peak in late November.

Capacity and Schedule Reliability

Port congestion across Southeast Asia remains elevated, with Singapore and Laem Chabang the main chokepoints (up to 9 days delay) and most other hubs, including Malaysia, Manila, and Vietnam, seeing 1–2 day waits due to high yard utilisation and vessel bunching.

Weather remains a watch point, with residual impacts from ex-Typhoon Fengshen still tracking through Vietnam and likely to create further scheduling ripple-effects.

Space conditions are tightening in parallel with early peak-season demand, and the next 3–4 weeks are expected to be the most challenging as vessels departing now are the ones arriving in AU for the Christmas/New Year window.

ASIA: Bottom Line

Both North and Southeast Asia are now in true peak-season conditions. Rates remain elevated and firm, space is heavily constrained, and congestion across hubs such as Singapore, Laem Chabang, and key Chinese ports is intensifying. Schedule reliability is under pressure as carriers roll cargo, skip ports, and adjust rotations to recover timetables following weather-related delays from ex-Typhoon Fengshen.

Over the next 3–4 weeks, expect the tightest capacity window of the year. Sailings departing now are those arriving into Australia pre-Christmas and pre-CNY cut-offs, meaning booking discipline and proactive planning are essential. Airfreight is also tightening in parallel, with urgent cargo already shifting off the water.

ASIA: Action Plan

Book early: Secure space at least 2–3 weeks before ETD. Both NE and SE Asia lanes are full through mid-November.

Choose services wisely: Use mid or premium tiers for time-critical or high-value cargo. From NE Asia, choose premium for guaranteed uplift. From SE Asia, select faster routings to avoid feeder delays.

Lock in delivery deadlines early: Provide required “on-site by” dates upfront so we can match routing (ocean, air or hybrid) to lead-time certainty.

Build for schedule disruption: Expect ongoing port/feeder delays and weather-driven instability - maintain buffer inventory where possible to absorb slippage.

USA/Canada: Market Overview

Ocean Freight Rates

The US market is currently experiencing a tactical rate rebound rather than a demand-led recovery. Spot rates have climbed sharply following mid-October GRIs - now sitting around USD 2,100/FEU to the West Coast and USD 3,100/FEU to the East Coast - driven by capacity restrictions and aggressive blank sailings, not a surge in underlying volume.

Capacity and Schedule Reliability

Capacity on the Trans-Pacific has improved on paper but remains tightly managed. Carriers continue to hold utilisation high through blank sailings and controlled allocations, keeping the market balanced despite subdued demand. Space is available, but not freely available. Priority is given to early bookings, with late cargo facing greater rollover risk as carriers defend rate levels.

Schedule reliability has lifted from Q3 lows but remains below historical norms, with vessel bunching and congestion still visible across key US gateways following erratic post-Golden Week departures. The reinstatement of additional sailings in November will lift nominal capacity, but carrier behaviour suggests this will be used to steady pricing rather than drive competition.

Importers front-loaded cargo ahead of the potential 1 November tariff shift, briefly lifting bookings, but forwarders continue to report ample space. Utilisation is expected to normalise at around 84–86% through November, up from 60–70% during Golden Week, while pricing strength remains supported by carrier discipline rather than demand recovery.

USA/CANADA: Bottom Line

The Trans-Pacific market is operating under managed capacity rather than genuine demand growth. Rates are holding firm because carriers are controlling space and timing GRIs, not due to a rebound in volumes. Capacity will improve into November but remain carefully curated, meaning uplift certainty depends more on booking timing and service tier than on price. Reliability has improved but remains uneven, with blank sailings, bunching, and port congestion continuing to disrupt arrival schedules.

USA/CANADA: Action Plan

Book earlier than usual: Secure uplift at least 2–3 weeks ahead of ETD to avoid being pushed to later vessels when space tightens.

Select routing based on speed, not price: Where possible, choose stable or direct rotations - the small price difference is outweighed by reduced rollover risk.

Plan for ongoing GRIs: Another increase is already signalled for early November; lock in rate validity where available to avoid escalation.

Monitor inventory timing: If cargo is tied to pre-holiday or tariff-sensitive windows, treat uplift as time-critical rather than opportunistic.

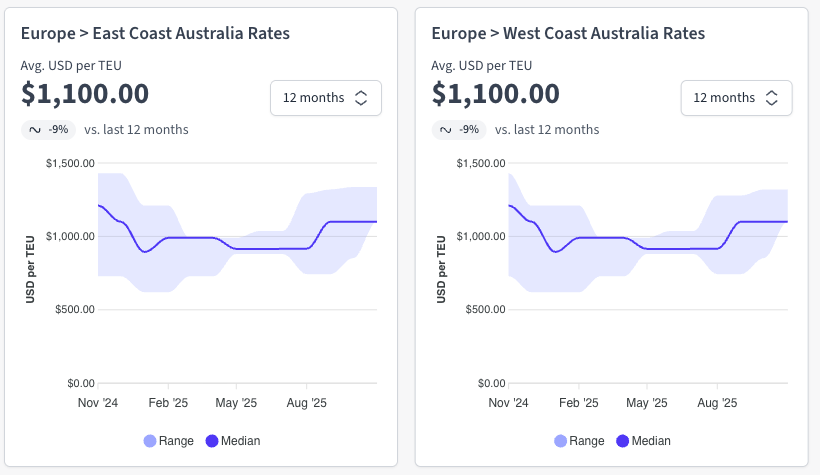

Europe: Market Overview

Europe is currently operating under a two-speed market: westbound exports (TAWB) face operational headwinds, with congestion and yard utilisation pressure across Antwerp, Rotterdam, Hamburg, and South Med hubs driving 2–8 day berth delays, while inland chassis/container shortages in Central and Eastern Europe continue to restrict fluidity. Despite this, spot rates remain soft at USD 1,800–1,900/FEU, reflecting subdued demand.

On the eastbound leg (FEWB), capacity remains ample and demand is still weak post-Golden Week, with carriers deploying blank sailings and strict space control to protect utilisation at ~80–85%. Rates have stabilised after a Q3 decline, supported by tighter capacity management rather than volume growth, and equipment is broadly available aside from pockets of 40’ shortages in South China.

Ocean Freight Rates

Westbound export rates (TAWB) remain soft at USD 1,800–1,900/FEU, reflecting muted demand despite ongoing congestion and inland bottlenecks across key hubs. Eastbound (FEWB) rates have stabilised following a Q3 correction, holding steady under tight capacity management rather than renewed demand.

Carriers continue to blank sailings selectively to keep utilisation around 80–85%, with limited signs of genuine volume recovery ahead of year-end.

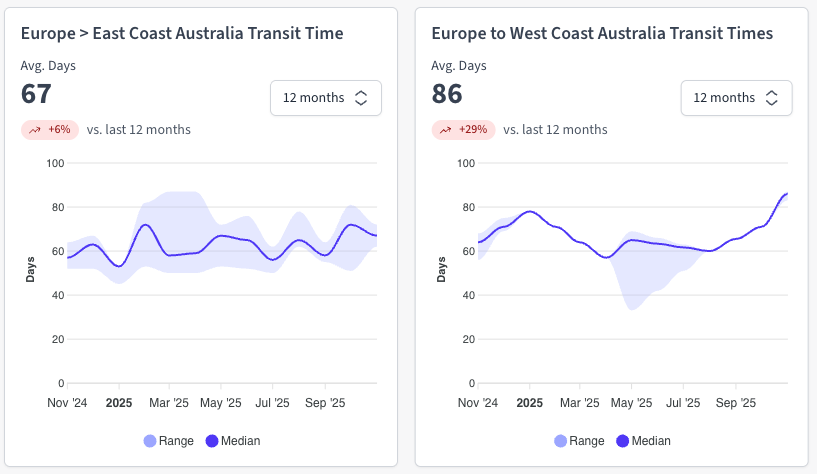

Capacity & Schedule Reliability

Northern Europe has come under significant operational strain over the past week, with Storm Benjamin forcing partial shutdowns across major gateways, including Rotterdam, Belgium (Antwerp), Felixstowe, and Valencia. The storm coincided with ongoing labour-related recovery delays, meaning the region is dealing with both weather disruption and backlog from last week’s strikes.

Antwerp, Rotterdam, and Wilhelmshaven are all posting elevated yard utilisation and slower landside throughput, while Hamburg is struggling with reduced berth capacity due to construction and technical rail issues impacting connectivity.

In France and the UK, Le Havre and London Gateway are still experiencing extended wait times and weather-related service interruptions, with Southampton also congested as late-arriving vessels bunch outside their window.

To stabilise schedule reliability on the Europe–Australia corridor, an 18th vessel has been added to the MSC Australian Express / CMA CGM NEMO service, phasing in from London Gateway on 15 October. The extra ship is designed to restore the weekly rhythm that was lost after the service was forced to reroute around the Cape of Good Hope due to Red Sea disruption. By expanding the rotation, carriers can absorb extended transit times without resorting to port omissions or heavy cut-and-run strategies. The vessel being deployed also offers higher deadweight, providing better lifting capacity for Australian export cargo and improved operational resilience across the rotation.

Overall, European reliability remains fragile, and recovery will likely be staggered, with ripple effects expected across feeder, barge, truck and rail flows into early November.

EUROPE: Bottom Line

The extra vessel on the Europe–Australia rotation is essentially a stability measure introduced to counter ongoing disruption across the European port network, not a capacity expansion in the traditional sense. With Northern European gateways still facing weather-related stoppages, labour backlog, yard congestion, and inland rail constraints, carriers are using the additional ship to absorb schedule shock caused by longer Cape-of-Good-Hope routings and congested port calls. This means fewer port omissions, lower rollover risk, and a more consistent weekly product - but transit times will still be extended, and demand softness on the Europe export leg won’t translate into price relief. Europe remains a reliability challenge rather than a rate challenge.

EUROPE: Action Plan

Plan around delayed but more predictable arrivals: The extra vessel improves schedule consistency, not speed. Build the extended Cape routing into lead times rather than assuming recovery.

Book early to secure uplift on stable windows: With congestion still elevated at Antwerp, Rotterdam, and Hamburg, forward bookings reduce exposure to berth delays and feeder interruptions.

Expect inland disruption to linger: Rail and chassis shortages in Central/Eastern Europe will continue to constrain container availability - locking in equipment earlier helps avoid last-mile bottlenecks.

Air Freight: Market Overview

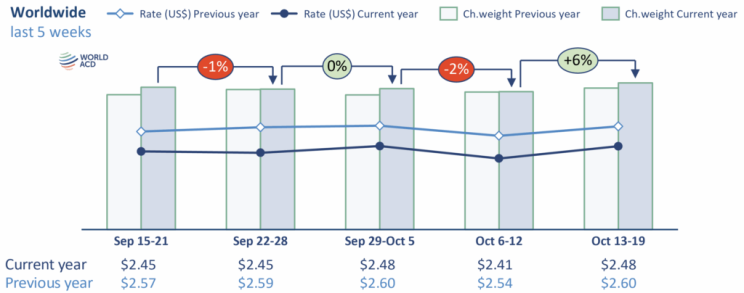

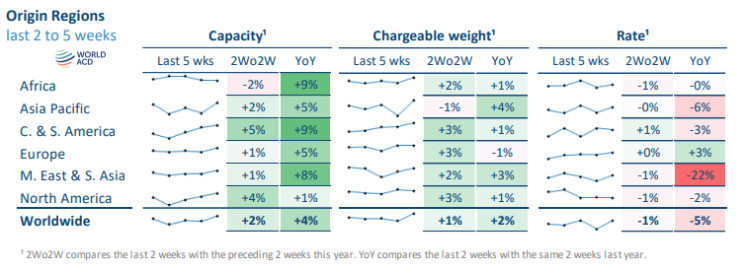

According to the latest WorldACD data for week 42 (13–19 October), global air-cargo tonnages rebounded by +6% week-on-week, led by a strong +14% lift from Asia-Pacific origins as the post-holiday lull faded. Meanwhile, average worldwide air-freight rates ticked up around +3% to US$2.48 per kilo, driven by higher-yield Asia-Pacific cargo. Importantly, spot rates from Asia to the US jumped +7% WoW, with China‐origin spot crossing ~$4.90 per kilo, its highest since mid-April.

AIR FREIGHT: The Bottom Line

The air-freight market is showing renewed momentum - particularly out of Asia-Pacific - signalling that the soft patch generated by holiday and tariff disruptions is fading. For importers into Australia, this means that air-rates are no longer in free-fall; instead, we’re entering a firming environment where capacity is tightening and pricing is re-normalising. Planning discipline now counts more than ever.

AIR FREIGHT: Action Plan

Book earlier and secure uplift windows: Forward-book space before demand spikes further. Last-minute bookings will increasingly default to higher-yield services or waitlisting.

Prioritise direct routings: Where available, select nonstop or single-stop routings to avoid transhipment risk, extended dwell time, and weather-related disruption.

Match product urgency to service type: Time-critical cargo should move on premium or express products; general cargo can still utilise deferred options, but with longer lead times.

Global Shipping Overview

The global logistics market is shifting from complacent softening into a cautious up-cycle: carriers are reasserting control, rates are stabilising or ticking upward, and lingering congestion and weather disruptions are exacerbating capacity tightness. While demand isn’t roaring back, sentiment has turned more confident - shippers are now planning on “space certainty over rate savings”.

In short: the window for opportunistic bargain hunting is closing, and we’re entering a phase where early, firm decisions matter more than chasing the lowest price.

Global Freight Rates

The latest World Container Index has risen by around 3% to USD 1,746 per 40ft, marking the second weekly increase after nearly four months of consistent declines. The uplift is broad-based, with Asia–US and Asia–Europe routes all recording rate increases - a signal that carriers are regaining pricing traction ahead of early-November GRIs and the lead-in to Q1 contract season. After a prolonged softening period, the market is now showing early signs of stabilisation and upward pressure, supported by improving load factors and tighter capacity controls. For importers, this suggests a shift from a falling-rate environment to a hold-or-climb outlook, reinforcing the need for earlier booking discipline and forward rate planning during peak-season liftings. Source: Drewry

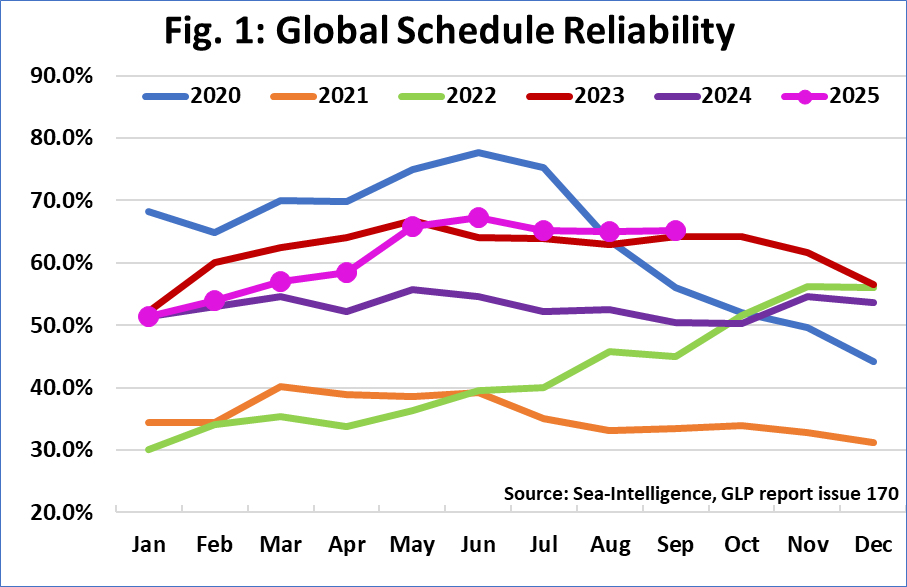

Global Schedule Reliability

Global schedule reliability has now levelled out in the mid-60% range, holding between 65–68% since May and sitting at 65.3% in August, signalling a plateau rather than continued improvement. Average late-arrival delays are still sitting at around 4.8 days, meaning performance is better than 2022/23, but still well below pre-COVID norms. At a carrier level, Maersk remains the most reliable globally at ~76%, followed by Hapag-Lloyd at around 72%, with most other major carriers clustered in the 60–70% range. The lower tier of the market still dips below 60%, with Wan Hai among those showing weaker schedule integrity. From an alliance perspective, the Gemini Cooperation is currently outperforming the wider market (close to 90% on certain trade arrivals), while older alliance structures continue to lag in the mid-50s. The overall takeaway: reliability has improved from last year’s volatility but has hit a ceiling - congestion, weather, industrial action and rerouted services (Red Sea/Cape) are preventing further gains. Source: Sea Intelligence

GLOBAL SHIPPING: The Bottom Line

This shift signals the end of the softening cycle and the start of a stabilising-to-rising rate environment, meaning shippers should not plan around price relief in the near term. Capacity is tightening across multiple Asian hubs at the same time carriers are re-asserting rate discipline, so uplift certainty will increasingly hinge on how early bookings are made, which service tier is selected, and how accurately delivery deadlines are communicated. In practical terms, the price gap between “budget” and “premium” matters less than the uplift risk - especially for time-sensitive inventory targeting pre-Christmas and pre-CNY arrival windows.

GLOBAL SHIPPING: Action Plan

Rates have stopped falling - and are now stabilising or rising: The recent uptick in the World Container Index confirms a structural shift away from the “declining rate” cycle. This is carrier-managed tightening, not demand-led inflation, but the outcome is the same: no meaningful price relief in the near term.

Capacity discipline is back in force: Blank sailings, ad-hoc service adjustments, and space rationing are now being used aggressively to protect load factors, particularly ex-Asia. This means even modest demand rebounds will translate into fast capacity tightening.

Congestion is creeping back via chokepoints, not everywhere at once: Singapore, Laem Chabang, Port Klang, and parts of Northern Europe are acting as bottlenecks - delays here cascade globally via feeder and transhipment timing, not just local port handling.

Weather + geopolitics remain the swing risks: Ex-Typhoon Fengshen impacts in Asia and ongoing Red Sea routing constraints continue to cause extended transit times. If either escalates, freight pricing could accelerate beyond current baselines.

Meet our Reports Builder

Our new Reports Builder feature allows you to turn your supply chain data into real insights. Here's why you'll love it.

Build it your way: Start with a ready-made report or create your own from scratch. Link data, add filters, and customise columns.

Set and forget: Schedule reports straight to your inbox (or your team’s) — daily, weekly, or monthly. Skip the manual work and get the insights automatically.

Turn data into insight: Bring together shipment and purchase order data to see the story behind the numbers. Spot delays, avoid detention, and keep freight moving efficiently.

The US and China have signalled a willingness to reset trade relations, with both sides working toward a new framework deal ahead of a high-stakes meeting between Xi and Trump. Markets are watching closely, as any breakthrough could ease tariff tensions - while failure would trigger another escalation cycle. Source: The Guardian

Cyclone Montha is intensifying over the Bay of Bengal and is expected to make landfall on India’s east coast late 28 October, bringing heavy rain (90-110 km/h gusts), high seas and flooding risk for coastal Andhra Pradesh, Odisha and Tamil Nadu. Authorities have issued red alerts, evacuated tens of thousands of residents and mobilised disaster response teams, signalling significant disruption to shipping, port operations and inland logistics in the region. Source: Indian Express

Hurricane Melissa made landfall in Jamaica as a catastrophic Category 5 storm, the most powerful ever recorded on the island with sustained winds around 185 mph and storm surges up to 4 m, causing extensive flooding, infrastructure damage and power outages. Source: ABC

APM Terminals and the Alabama Port Authority are advancing a major expansion at the Port of Mobile - a project that boosts capacity, adds on-dock rail access and positions the port as a leading U.S. gateway. The investment underscores the port’s strategic shift to support larger vessels, deeper draft access and enhanced intermodal connectivity for container flows. Source: Splash 24/7

With decades of expertise improving supply chains across Australia and the globe, I know what insights businesses need to stay proactive and ahead of disruption. Consider this your go-to resource for staying informed and making smarter logistics decisions. Get yours in your inbox - subscribe via LinkedIn or get in touch.

Be the first to know

No spam. Just the latest market news, tips, and interesting articles in your inbox.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

.jpg)