Got a tracking number? Let’s see where your freight is

Victoria International Container Terminal (VICT) has temporarily closed its gates on 1st September, due to a large pro-Palestine protest at Webb Dock. Police are on site managing the situation, but at this stage, there’s no clear timeframe on when operations will resume. Source: FTA

Victoria’s logistics network is set for a boost with the release of the Victorian Freight Plan 2025–2030. The plan, developed with input from the Port of Melbourne, builds on previous strategies while addressing recent industry challenges, including global disruptions, decarbonisation, and increasing demand for cleaner freight solutions. Key goals include reducing red tape, supporting modal shifts, attracting private investment, and leveraging technology to improve network performance. Port of Melbourne CEO Saul Cannon highlighted the importance of aligning government and industry to create a safer, smarter, and more sustainable supply chain.

Seasonal high winds are impacting empty yards locally, with SA, VIC and NSW most affected. This can flow through to port rotations as lines work on schedule reliability.

Brisbane has experienced several short-term disruptions across Hutchison Ports and DP World in recent weeks. Hutchison faced industrial action on 21 August, causing minor delays, while DP World has dealt with IT system maintenance, technical issues with Automated Stacking Cranes, ICT network instability, and adverse weather impacts on truck turnaround times. To mitigate delays, DP World has introduced manual handling workarounds, a new stacking yard, and additional resourcing for breakdown response.

It’s often the more agile carriers who set the tone. With a focus on spot FAK cargo and smaller fleets, they flex their pricing quickly to fill capacity. When the market is soft, they cut rates to stimulate demand. But when space tightens, they move first and decisively to push rates up, often vessel by vessel. In contrast, carriers with large NAC/BCO contract portfolios (50–60% tied up long term) react more conservatively, limiting volatility but still following the market’s overall direction.

The second half of August reflected this dynamic perfectly. Rates began soft, carriers pushed higher mid-month, then eased, before surging again as peak season demand hit. By late August, space shortages in Shenzhen and other South China ports saw containers rolled repeatedly, sometimes across two sailings, pushing spot rates sharply upward even before September.

This year, three key factors underpin a steadier, more resilient rate climb:

In short, rates are rising steadily, capacity is tight, and the China–Australia lane is firmly in peak season mode. Unless we see a sudden influx of ad-hoc tonnage, this momentum is likely to hold through September and October.

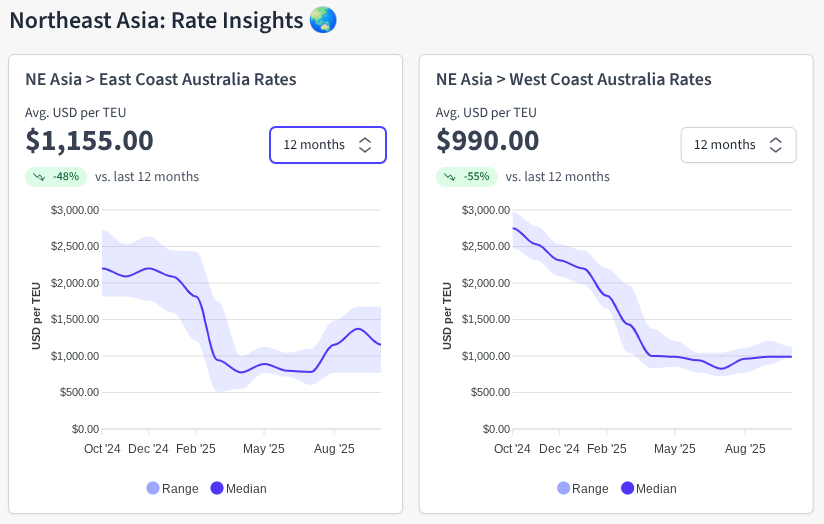

Current market rates from major Chinese ports to the Australian East Coast show a range of competitive pricing across carriers. Rates as low as USD 1,300 per TEU are available, with several services meeting the market at around USD 1,400 per TEU.

Some carriers have adjusted their offerings, bringing rates down to USD 1,450 per TEU from previously published levels of USD 1,550 per TEU. Others are maintaining pricing around USD 1,500 per TEU, providing reliable transit options including faster routes to Brisbane.

Meanwhile, select carriers have introduced further rate increases, now quoting USD 1,650 per TEU. These services are currently experiencing strong demand, with high vessel utilisation and frequent rolling.

The Fremantle/Adelaide trade has seen stable vessel deployment since April, with no significant changes reported. However, ongoing cargo congestion in Singapore, along with upward pressure on rates in the East Coast trade, has led to increased pricing for the West Coast corridor, now reaching USD 1,100 per TEU.

A new port call in Melbourne commencing in September has added stability to a direct West Coast service, supporting rate alignment with broader market trends.

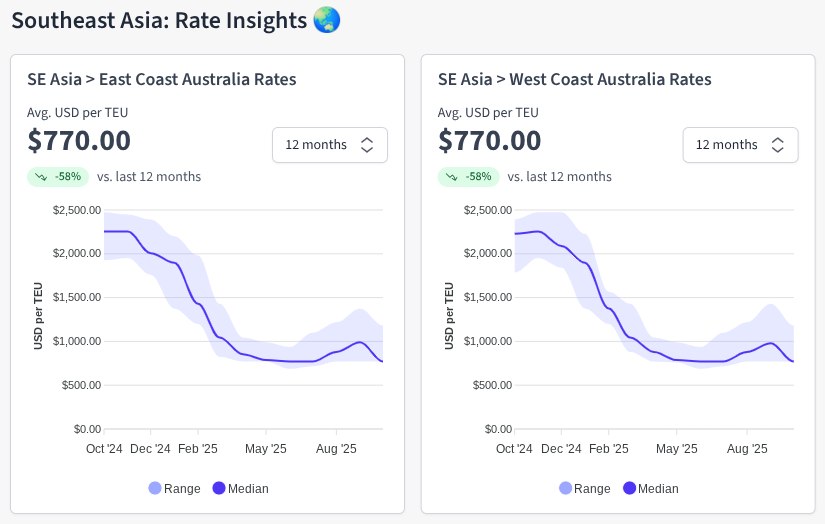

Rates ex South East Asia saw another increase in September.

ANL / Swire / PIL have announced a new direct service from China to PNG.

ANL (APR2)

Routing: Qingdao → Busan → Shanghai → Ningbo → Nansha → Lae → Motukea, PNG → Brisbane → Gladstone → Townsville

Vessel capacity: 1756 TEU per vessel, and ANL will operate 3 vessels on this service.

First sailing: San Giorgio, ETD Qingdao 12/Sep.

Frequency: Biweekly

Swire/PIL (NAX / ANA)

Routing: Shanghai (Wednesday) → Ningbo (Saturday) → Nansha (Wednesday) → Hong Kong (Thursday) → Lae → Port Moresby → Townsville

Vessel capacity: 2800 TEU per vessel, and they will operate 3 vessels on this service.

First sailing: Lae Chief, ETD ETD Shanghai: 22/Aug

Frequency: Biweekly

Extra loaders are being released for September as follows:

PIL: Kota Neka - 1810 TEU

TAO 05/Sep - NGB 08/Sep - HKG 11/Sep - BNE 23/Sep - LAE & POM 26/Sep

MSC: MSC Lucia III - 2556 TEU

SHA 08/Sep - NGB 09/Sep - YTN 12/Sep - BNE 21/Sep - SYD 23/Oct

TSL: TS Xiamen 2514S - 1909 TEU

SHK 13/Sep - NSA 14/Sep - BNE 26/Sep - SYD 29/Sep - MEL 01/Oct

TSL: TS Chennai 2505S - 2954 TEU

XGG 15/Sep - TAO 16/Sep - SHA 18/Sep - NGB 19/Sep - SHK 22/Sep - NSA 23/Sep - BNE 06/Oct - SYD 09/Oct - MEL 11/Oct

TSL: TS Tokyo 2513S - 1787 TEU

SHK 25/Sep - NSA 26/Sep - BNE 09/Oct - SYD 12/Oct - MEL 14/Oct

The CAT service will have a blank sailing in week 39.

The Wallaby service will have a blank sailing in week 35.

Week 35 - OOCL Kuala Lumpur V183S - delayed by 4 days.

Week 36 - Cosco Rotterdam V203S - delayed by 4 days.

Week 35 - MSC Barbara KQ523A - delayed by 4 days.

Week 35 - MSC Unity KQ531A - delayed by 13 days.

Week 36 - Kota Lawa V98 - delayed by 5 days.

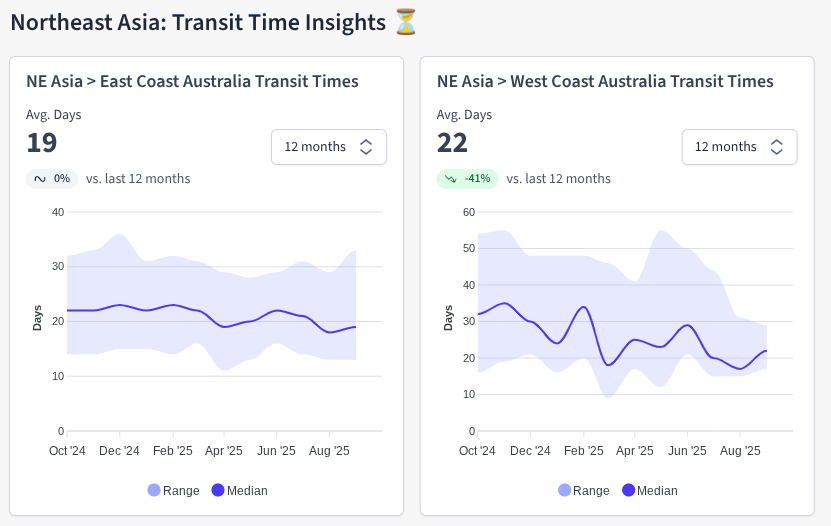

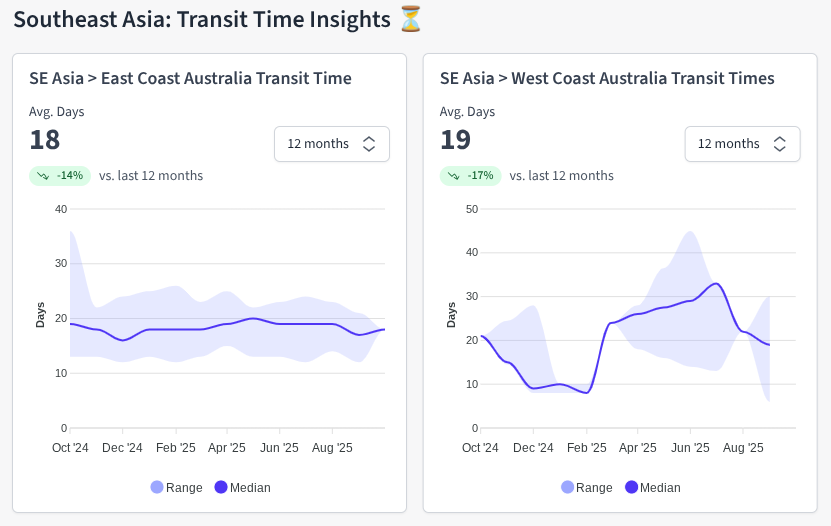

Ex-China remains highly challenging, with Shanghai, Ningbo, and Qingdao experiencing the most disruption. Despite booking months in advance, containers continue to be rolled, often after being gated in, leaving little flexibility to pivot to alternatives. Carriers are consistently overbooking, resulting in many containers being pushed to subsequent vessels. Southeast Asia is facing similar pressures, with Penang particularly impacted, and feeder congestion is now evident ex-Thailand, Vietnam, and Malaysia as carriers struggle to connect cargo to mainline vessels.

Transhipment delays are also widening. While previously concentrated in Singapore and Port Klang, congestion has now spread to Tanjung Pelapas as carriers divert routings to avoid SIN/PKG. In some cases, intended transhipment ports appear “blank” in tracking, meaning ETA accuracy cannot be relied upon until confirmed by carriers. Additionally, port omissions and rotation changes are increasing as lines attempt to recover schedule delays or bypass congestion/weather. While some carriers proactively communicate these adjustments, others do not.

Luckily, our app offers accurate tracking.

Due to the bad weather, ANL ROTORUA V. 2517 is currently taking shelter in Huraki Gulf. Thereafter, the vessel is planning on taking a longer route to avoid bad weather.

To minimize the delays, ANL ROTORUA V. 2517 will be calling AUMEL prior to AUSYD.

Due to weather issues in Asia and port congestion in Australia, ALS LUNA 001N/002S will have to omit Pusan call in order to assist with her schedule recovery.

To avoid further delays and to assist in schedule recovery, EXPRESS BLACK SEA 069N/070S will omit PORT KELANG.

Below is the updated schedule for reference.

FRE – 04 Sept

PKG – OMIT

SIN – 13 Sept

FRE – 22 Sept

OOCL CANADA has been severely impacted by an adverse weather event in Asia and in order to assist with her schedule recovery, OOCL CANADA voyage 115N/116S will omit Xiamen call.

Average vessel waiting time has improved slightly to 2.24 days, but berthing delays continue across CCT, CGB, and NCT. Gearless vessels are facing 3–5 days of delay, while geared vessels wait 1–3 days. Yard occupancy remains tight at 90%.

Severe weather is disrupting port operations, with India’s Meteorology Department issuing a Red Alert for Mumbai, Thane, Raigad, and Palghar (19–21 August). Vessel movements at Nhava Sheva are suspended, and delays are building across container yards, CFS, and transit routes. Both road and rail are heavily impacted by waterlogging, with highways and train lines submerged.

Upcoming Public Holidays

TPEB: The Peak Season Surcharge (PSS) was removed for the fixed market during August and will remain off until mid-September, though some carriers have announced a return from September 15. A General Rate Increase (GRI) was announced for September 1, but with current overcapacity and softening demand, its implementation is still uncertain.

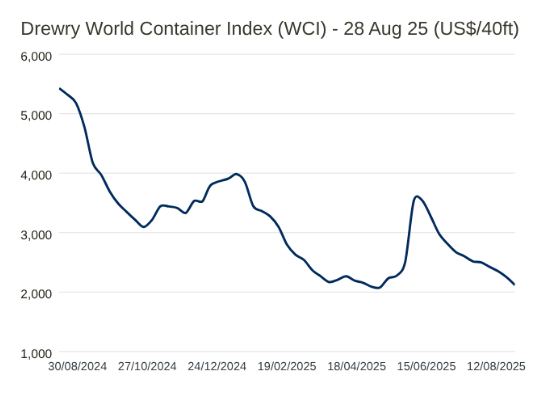

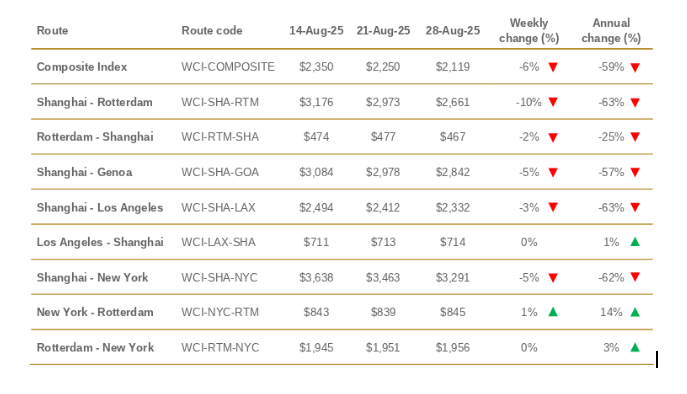

Drewry’s World Container Index (WCI) has now fallen for the 11th week straight, with further declines expected. The turbulence started back in April when US tariffs were announced, rates spiked through May and early June, only to tumble from mid-July right up to this week. Transpacific spot rates slipped again, with Shanghai–Los Angeles down 3% ($2,332/FEU) and Shanghai–New York down 5% ($3,291/FEU). The early peak season, driven by front-loaded retail orders, has wrapped up. Now, with a slowing US economy and higher tariff costs, retailers are easing back on procurement, steady but cautious. Drewry expects this lane to keep sliding in the weeks ahead. Source: Drewry

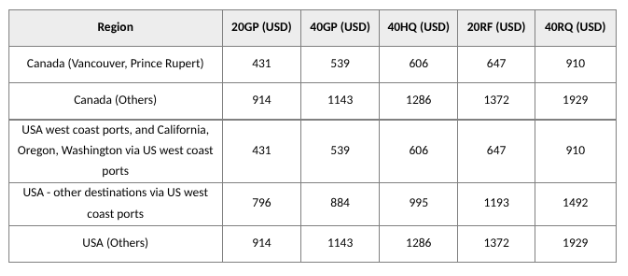

AU Export to USA - OOCL will implement a Fuel Cost Recovery (FCR) from Australia, New Zealand to Canada, USA destinations, with effect from 1st October 2025.

US west coast ports include Tacoma, WA / Oakland, CA / Long Beach, CA / Seattle, WA / Los Angeles, CA.

TPEB: As we approach Golden Week, the market isn’t expecting a major spike in demand. Many shipments were pulled forward earlier in the year to beat potential tariffs, leaving the summer relatively quiet and suggesting a muted fall. September capacity is sitting at 80–90% of normal levels, and space remains widely available, with demand still lagging behind. Equipment availability has improved slightly since late July. While carriers like CMA and HMM continue to experience equipment tightness, most other carriers are seeing healthier conditions.

No major disruptions are being reported at this stage. Transit times remain stable, and carriers are largely maintaining their schedules, though the usual peak season congestion could emerge if demand suddenly increases or Golden Week volumes concentrate.

Asia–Europe spot rates also softened this week. Shanghai–Rotterdam dropped 10% ($2,661/FEU), while Shanghai–Genoa slid 5% ($2,842/FEU). Even with strong demand and ongoing port delays, an oversupply of vessel capacity continues to weigh on the market. Drewry is forecasting further downside for rates here as well.

FEWB: The Shanghai Containerized Freight Index (SCFI) continued its decline last week, dropping to USD 1,668 per TEU, marking the fourth consecutive week of falls. While September blank sailings will tighten overall capacity, early factory closures ahead of Golden Week will put pressure on carriers to fill vessels, which may gradually weigh on freight rates. Volumes have remained relatively steady following the traditional peak, which could moderate the pace of rate declines through September.

TAWB: Demand remains firm, and load factors are stable. Spot rates from North Europe to the U.S. East Coast are currently around USD 1,900–2,000 per FEU. Peak Season Surcharges (PSS) have been deferred, with rate extensions in place through September for North Europe, East Mediterranean, and West Mediterranean.

FEWB: September blank sailings are expected to cut weekly capacity by around 10% in the first half of the month. Congestion at destination ports remains a challenge, which may extend transit times over the coming weeks. From origin ports, space availability has improved since August, and equipment supply has returned to normal. Despite this, we still recommend booking 2–3 weeks ahead of your intended departure. With the traditional pre-Golden-Week demand surge approaching, securing space as early as possible is strongly advised.

TAWB: Yard utilization remains high across major European ports. Antwerp continues to experience heavy congestion, with yard occupancy above 90% and dwell times around seven days. Rotterdam, Hamburg, and Bremerhaven are seeing 75–95% yard utilization, with vessel delays of 2–3 days. Ports in the South Mediterranean, Piraeus, Genoa, and Valencia, remain congested, with vessel delays extending 3–6 days.

FEWB: Transit times at destination ports may remain extended due to ongoing congestion. Overall, schedules are being maintained, but delays could emerge if port bottlenecks intensify or volumes concentrate ahead of Golden Week.

CMA CGM hereby inform you that due to an operational constraint, M/V MSC AJACCIO 0NNM5E1MA will omit HAMBURG.

Antwerp terminals remain heavily congested, with reduced labour availability impacting both landside and waterside operations. Productivity continues to be affected, and vessel turnaround is slower than usual.

Bremerhaven: Rail service disruptions caused by a significant accident between Bremen and Bremerhaven are limiting capacity. Delays for services to and from the port are expected until repairs are complete.

Hamburg: Port operations continue to face challenges from construction, labour shortages, and other disruptions.

Genoa: Some carriers are skipping the port due to congestion, high yard utilisation, and limited labour availability.

Rotterdam:

Rhine River: Water levels have improved across all measuring points, and previous barge capacity restrictions have been lifted.

Algeciras: Yard density sits around 83%. TTIA continues using a dynamic berth model prioritising loading-heavy vessels to maintain flow. Valencia: Vessel bunching has resulted in an average waiting time of 3 days. Yard density is high at 82%, and gate congestion is affecting cargo collection.

In July 2025, global schedule reliability slipped month-on-month for the first time since January, falling -2.2 percentage points to 65.2%. Year-on-year, however, reliability remained stronger, up 13.0 percentage points. Average delays for late vessel arrivals also worsened slightly, increasing by 0.14 days to reach 4.68 days.

Among the top-13 carriers, Maersk led with the highest reliability at 80.6%, followed by Hapag-Lloyd at 74.0%. Six carriers fell within the 60–70% range, while the remainder trailed in the 50–60% bracket. HMM recorded the lowest reliability in July, at 50.7%. Source: Sea Intelligence

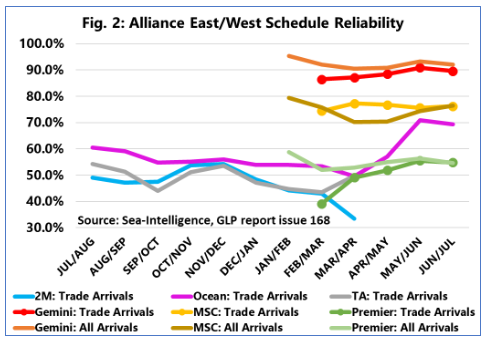

Traditionally, alliance performance has been measured by arrivals into destination regions. But since that data wasn’t available for the new alliances back in February, a new metric was introduced that also captures origin region calls on the East/West trades. For now, both measures are reported – “All arrivals” (aligned with the February metric) and “Trade arrivals” (aligned with the previous alliance structure). Over time, as the new alliances settle in, the two measures will converge.

For June/July 2025, Gemini Cooperation led the way with 92.0% reliability on all arrivals and 89.6% on trade arrivals. MSC followed at 76.5% and 76.2% respectively, while Premier Alliance lagged at 54.6% and 54.8%. For the “old” alliances, both measures are equal, with Ocean Alliance recording 69.4%.

Source: Sea Intelligence

Drewry’s World Container Index (WCI) has now logged its 11th consecutive weekly decline, with no signs of stabilising in the near term. What began as a tariff-driven surge earlier this year has shifted into a prolonged correction, as both US and European lanes show sustained downward pressure on spot rates. The global supply–demand balance is expected to soften further in 2H25, with the trajectory largely dependent on geopolitical factors and capacity shifts.

Source: Drewry

Globally, Drewry’s Container Forecaster projects that supply–demand dynamics will weaken again in the second half of 2025, leading to additional rate contractions. The scale and volatility of these shifts will hinge on two key uncertainties: future US tariff policies and potential capacity disruptions tied to penalties on Chinese vessels.

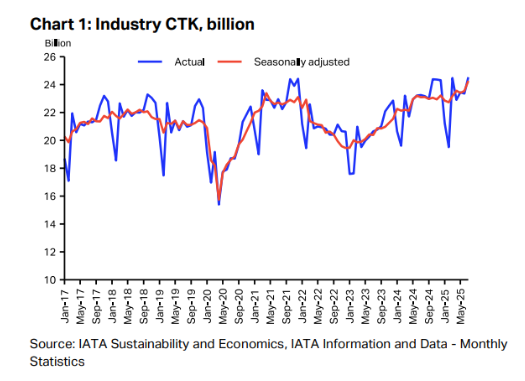

In July 2025, global air cargo demand rebounded strongly, with Cargo Tonne-Kilometers (CTK) increasing by 5.5% year-on-year (YoY), up from just 0.6% in June. This surge was primarily driven by shippers accelerating shipments ahead of anticipated U.S. tariffs, leading to a frontloading of goods into the air cargo system. Asia-Pacific carriers led this growth, reporting an 11.1% YoY increase in demand, the highest among all regions. However, the Asia–North America trade lane experienced a 1.0% decline, marking its third consecutive month of negative growth.

For Australian importers, this uptick in global air cargo demand could translate to increased competition for available capacity, potentially leading to higher freight rates and tighter space, especially on high-demand routes. While capacity increased by 3.9% YoY, the rise in demand outpaced capacity growth, resulting in a 0.7 percentage point increase in the global Cargo Load Factor (CLF) to 45.1%. This tightening of capacity may impact shipping schedules and delivery timelines. Additionally, the expiration of U.S. de minimis exemptions on small shipments has led to a decline in e-commerce volumes, particularly affecting the Asia–North America corridor. Australian exporters to the U.S. may need to adjust their strategies to mitigate these changes.

Looking ahead, the ongoing uncertainty surrounding U.S. trade policies and the potential for further tariff adjustments could continue to influence global air cargo dynamics. Australian businesses should consider these factors when planning their logistics and supply chain strategies to navigate the evolving market conditions.

Source: IATA

Vietnam is bracing for Typhoon Kajiki, the strongest storm of the year, as it approaches the central coast with winds reaching up to 166 km/h (103 mph). Authorities have ordered the evacuation of over 500,000 residents, shut down airports in Thanh Hoa and Quang Binh, closed schools, and canceled flights. Military and paramilitary forces, numbering more than 123,000 personnel, have been mobilized to assist with evacuation and rescue operations. The storm, expected to cause heavy rainfall, flooding, and landslides, is also impacting neighboring China: Hainan Island’s Sanya City has closed businesses and transport services, though emergency alerts there have now been downgraded.

Source: BBC

With decades of expertise in fixing and improving supply chains across Australia and the globe, I know what insights businesses need to stay proactive and ahead of disruption. Consider this your go-to resource for staying informed and making smarter logistics decisions. Get yours in your inbox - subscribe via LinkedIn or get in touch.

No spam. Just the latest market news, tips, and interesting articles in your inbox.