Container shipping is entering a softer cycle as we move into December. Fleet capacity is still growing faster than demand, and while carriers are managing schedules with blank sailings, volatility remains centred around key hubs such as Singapore.

Global Ocean Freight Market trends

For oceania shippers: Early planning for December-January closures and Chinese New Year will be essential to maintain flow.

Port operations across Australia remain under pressure. Weather, vessel bunching, transhipment congestion and ongoing port omissions continue to affect schedule reliability.

Conditions are expected to remain challenging over the next 3-4 weeks as sailings target both pre-Christmas and pre-CNY arrivals.

Brisbane: Delays:

Delays: ~2-5 days

Remains relatively steady, though vessel bunching is causing intermittent yard pressure. Last week’s DP World power outage temporarily halted four cranes; operations have mostly recovered but minor flow-on disruptions remain. Booking and receival windows are open, but filling quickly.

Sydney: Delays:

Delays: ~5 days

High winds and continued vessel bunching are slowing productivity and increasing omission risk. The recent DP World stop-work meeting contributed to the backlog, with residual effects still working through the system.

Melbourne: Delays:

Delays: ~2 days

Yard density is still elevated and truck turnarounds are slower than usual. Late-cutoff cargo is at increased rollover risk. Conditions should stabilise as labour availability returns to normal levels.

Fremantle: Delays:

Delays; 4-7 days

Fremantle is feeling upstream impacts from east-coast congestion and schedule compression. Omission risk remains elevated. Tight berthing windows and congestion from Singapore continue to push delays downstream.

Adelaide: Delays:

Delays: 3 days

Remains the most stable port nationally. Minor delays occur when absorbing cargo diverted from omitted calls. Most issues are driven by upstream schedule recovery rather than local congestion.

Other notes:

Reefer and 20ft equipment tight across most terminals.

NZ rail maintenance around Auckland/Tauranga has reduced trans-Tasman efficiency, causing minor flow-on delays.

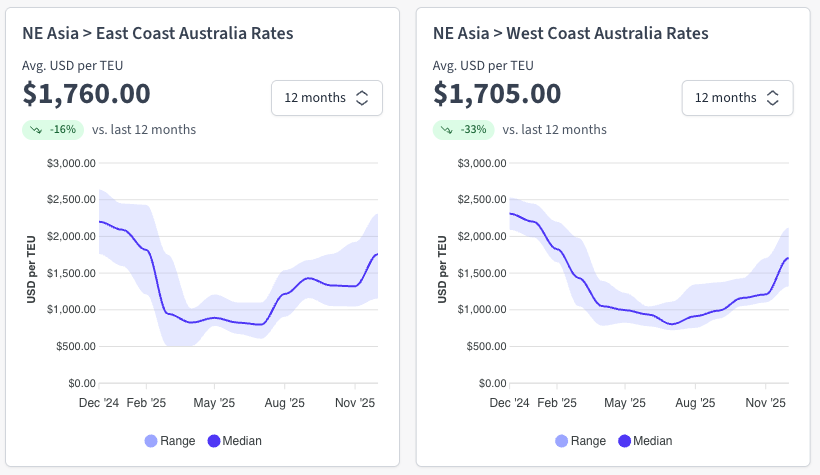

North East Asia: Freight Market Overview

The NE Asia market remains firm heading into late November. Rates are holding across all service tiers and space remains tight, driven by steady export demand and persistent congestion at key transhipment hubs. Carriers are managing capacity through selective blank sailings and controlled service rotations, slowing schedule recovery and limiting available space into Australia.

These conditions are expected to continue into December. Shippers should plan around December–January shutdown periods and begin securing uplift early ahead of Chinese New Year in mid-February.

Ocean Freight Rates

Click image to view live data

Budget Services: Approx. USD 1,300 / 2,600 from all major China ports to the Australian east coast.

Mid Tier Services: Holding around USD 1,400 / 2,800, with slight increases ex Tianjin and Dalian.

Premium Services: Sitting at USD 1,700 / 3,400, reflecting demand for guaranteed uplift, better schedule protection and faster turnarounds.

Capacity and Schedule Reliability

Click image to view live data

Ongoing congestion across North East Asia continues to impact schedule reliability

Singapore transhipment delays remain the main pressure point

Further blank sailings expected as carriers rebalance capacity through December

A widening imbalance between China’s exports and imports is absorbing more container capacity than expected, straining networks and limiting schedule flexibility as carriers reposition equipment to match outbound demand. Source: JOC

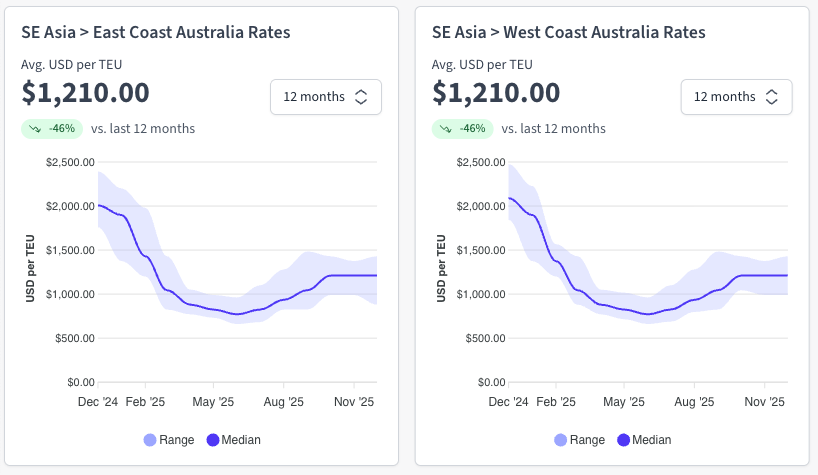

South East Asia: Freight Market Overview

Rates across SE Asia remain steady. Export demand is consistent, but reliability is being affected by equipment shortages, regional congestion and weather-related delays from recent typhoons. Singapore remains a transhipment bottleneck, creating variability in connections into Australia.

These conditions are expected to continue into December. Delivery timelines should be planned early where stock availability is critical.

Ocean Freight Rates

Click image to view live data

Budget Services: Around USD 900 / 1,800 across major SE Asia origins

Mid Tier Services: Holding at USD 1,100 / 2,200

Premium Services: Sitting higher at USD 1,300 / 2,600, driven by demand for faster connections and schedule protection

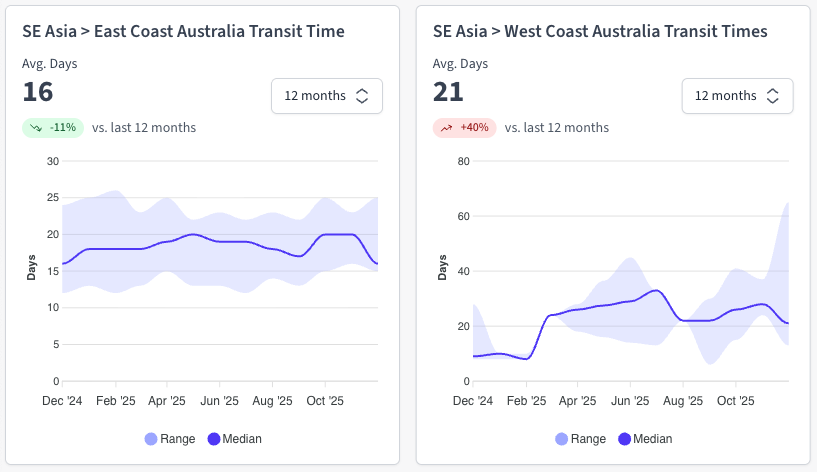

Capacity and Schedule Reliability

Click image to view live data

Recent typhoons have caused weather-related delays through parts of South East Asia.

Singapore’s transhipment backlog continues as congestion, vessel bunching and blank sailings disrupt network fluidity. This remains the most significant pressure point for AU-bound cargo connecting via Asia. Loadstar

ASIA: The Bottom Line

Asia remains tight but manageable. Rates are stable, but congestion and ongoing equipment constraints continue to affect connections into Australia.

December-January closures and early Chinese New Year demand will add pressure quickly. Early planning remains the best way to maintain flow.

ASIA: Action Plan

Share your December–January shutdown periods early

Firm bookings in the lead-up to Chinese New Year (mid-Feb) as space will tighten quickly across all tiers.

Plan delivery requirements in advance, especially where stock availability or tight delivery windows are critical.

Stay flexible on routes and service tiers where possible due to ongoing congestion and intermittent equipment shortages.

Coordinate with Operations/Transport teams to ensure uplift, transhipment timing and downstream delivery dates are aligned.

Freight Rates

The North America market remains soft heading into December, with stable pricing and generally open space into Oceania. Demand has eased, and while carriers are using blank sailings across some trans-Pacific lanes, overall capacity remains available. West Coast gateways are performing relatively well, while some East Coast and inland rail-linked hubs continue to experience intermittent congestion and longer dwell times.

Low End: USD 1,500 Per TEU

High End: 2,000 Per TEU

Capacity and Schedule Reliability

Capacity into Oceania from both the US and Canada remains generally healthy, with adequate space across West and East Coast gateways.

While some East Coast ports and inland rail hubs are still experiencing intermittent congestion, these delays have not had a material impact on overall uplift.

A small number of blank sailings are scheduled, but they're not expected to affect availability for Australia-bound cargo.

As temperatures continue to drop across parts of North America, BMSB fumigation is becoming harder to complete at origin, meaning some shipments may need treatment at transhipment hubs or on arrival.

USA/CANADA: Bottom Line

Favourable conditions for Oceania importers, with steady rates and good space availability. Schedule variability and BMSB compliance remain the main considerations.

USA/CANADA: Action Plan

Confirm fumigation options early

Allow buffer for East Coast and inland delays

Flag critical delivery dates with Operations

Use stable pricing to move time-sensitive cargo early

Europe: Freight Market Overview

European load ports continue to face congestion and longer dwell times, with carriers compressing schedules and adjusting rotations in response. Blank sailings are expected to continue into December.

For Australia-bound cargo, the main impacts are extended load-port dwell times and inconsistent transhipment connections through Singapore and Port Klang.

Ocean Freight Rates

Click image to view live data

Budget Services: Sit around USD 1,000 / USD 2,000

Mid Tier Services: Holding at USD 1,300 / USD 2,600

Premium Services: Sit higher at USD 1,600 / USD 3,200

Capacity and Schedule Reliability

Click image to view live data

Capacity ex Europe is available but unevenly deployed

European ports are facing prolonged congestion, exposing how limited terminal buffer capacity and inland transport availability are when vessel arrivals surge. The result is higher dwell times, rollover risk and service inconsistency across North Europe hubs. Source: Loadstar

This is flowing through to less predictable transhipment timings via Singapore and Port Klang for AU-bound cargo

The national strike in Belgium has disrupted port operations and increased congestion at the Port of Antwerp. This congestion is expected to worsen as a few carriers are planning to return to the Suez Canal route, which will further strain port efficiency, leading to longer delays and surging spot rates. Drewry

EUROPE: Bottom Line

Whilst rates remain steady for major European ports, schedule reliability and equipment shortages are still prevalent. In particular, there is a shortage of 20GP & reefer equipment at the moment.

EUROPE: Action Plan

Check equipment availability prior to making bookings.

Build extra lead time into forecasting to account for dwell times at origin, inconsistent transhipments & equipment availability.

Try and utilise carriers offering more direct sailings to AU.

Air Freight: Market Overview

US-bound ecommerce demand is easing after a brief “mini peak,” but Asia-origin airfreight remains tight with strong volumes, limited capacity and firm rates heading into December. Conditions are expected to ease only after early January. Loadstar

Capacity is tight across key origins including China, Vietnam, Korea and parts of Southeast Asia, with most direct and transit services heavily booked.

Most carriers continue to recommend 7–10 days’ lead time for time-critical freight, and premium services are seeing the highest pressure as shippers seek more reliable transit windows.

Conditions remain tight across Asia, and AU-bound capacity is expected to stay firm through December. While demand into North America shows signs of softening, the impact has not yet flowed through to improved uplift conditions for Australia. Expect limited flexibility on routings and continued pressure on transit times until early January.

AIR FREIGHT: Action Plan

Book 7-10 days in advance for time-sensitive or consolidated cargo.

Allow routing flexibility, as some hubs remain congested and schedules are running tight.

Consider premium uplift for urgent cargo where transit reliability is critical.

Share critical arrival dates early so uplift and connections can be planned around peak-season constraints

Nick Scali and Explorate win ASCL Award for data-driven supply chain innovation.

Earlier this month, our partnership with Nick Scali was recognised at the 2025 Australian Supply Chain and Logistics Awards in the Big Data, IT and Business Intelligence category.

A partnership that began following a challenging disruption for Nick Scali last year has grown into a rewarding and high-impact collaboration. In a matter of months, the two teams reengineered Nick Scali's global supply chain into one that sets the standard for visibility, control and performance.

Global freight markets are entering a softer phase as we approach the end of 2025. Demand seems to be lower than anticipated globally but ties in with the overall global economic environment.

Carriers are countering this with blank sailings, general rate increases, and tighter schedule management. Transhipment reliability, particularly through Singapore remains the most significant pressure point for Oceania-bound cargo.

Across Europe and North America, congestion, labour constraints and equipment shortages continue to create uneven schedule performance. For AU importers, the main impact is extended dwell times at origin and less predictable transhipment connectivity into Southeast Asia hubs. Despite these pressures, overall space availability remains reasonable across most long-haul trades, provided bookings are planned early and routing flexibility is allowed.

Looking ahead, Drewry expects global supply-demand conditions to weaken over the coming quarters, especially if Suez Canal transits return to normal and more capacity re-enters circulation.

Global Freight Rates

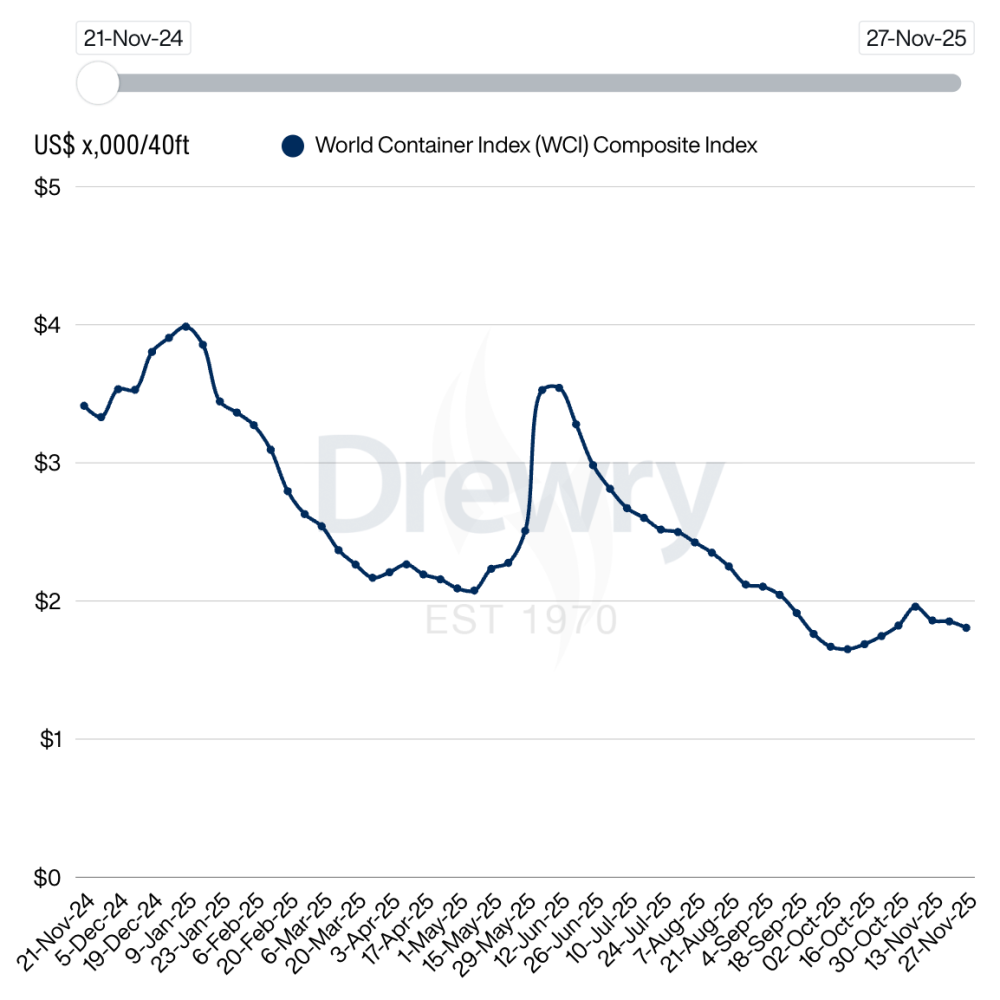

The Drewry World Container Index (WCI) decreased 2% to $1,806 per 40ft container. The decline was primarily due to reduced rates on the Transpacific and Asia–Europe trade routes.

Global Schedule Reliability

Global schedule reliability remains uneven, with the biggest delays concentrated in Singapore, North Europe hubs, and US East Coast ports.

Blank sailings and rotation changes continue to distort week-to-week vessel arrival patterns across Asia–EU and trans-Pacific networks.

Weather, congestion and equipment imbalances remain the main causes of missed connections and rolled cargo across multiple trade lanes

General News

Macquarie has made an A$11.6 billion all-cash offer to take Qube private. The bid has strong backing from major investors and could see Australia’s largest integrated logistics operator move into new ownership. Source: AFR

Trans-Atlantic capacity has hit its highest level in over two years as carriers add ships and demand softens, putting downward pressure on rates despite ongoing congestion at several major European ports. This imbalance is contributing to schedule variability on services connecting via Europe. Source: JOC

A containership fire at a major US port injured four crew members and caused temporary operational disruption, highlighting ongoing fragility in port infrastructure and the time needed to restore normal vessel scheduling when incidents occur. JOC

The UK’s delay in removing its de minimis threshold has raised concerns it could become a landing spot for low-value e-commerce imports. Loadstar

Overcapacity in container shipping is a key theme for the year ahead. Xeneta takes a look at the different ways carriers will tackle this problem across the world’s major trades. Xeneta